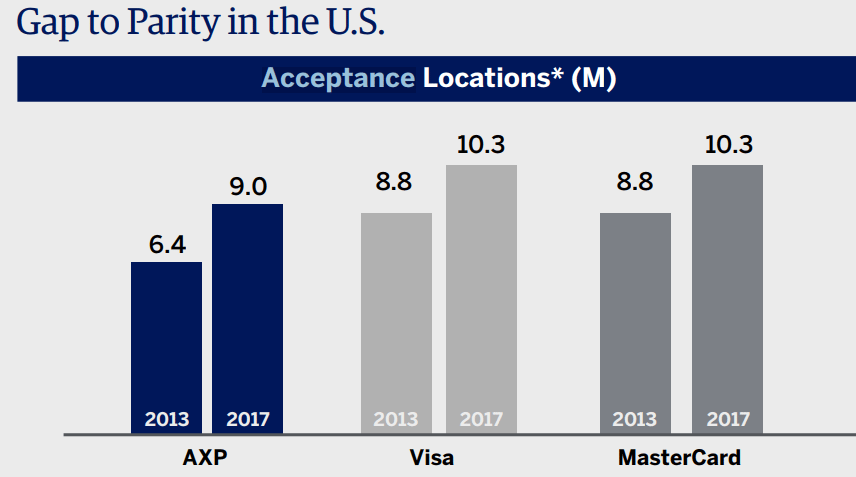

American Express has announced that it will lower the fees it charges merchants by the most it has done in the last two decades in an effort to increase American Express acceptance. Currently American Express is accepted at 1.3 million fewer locations than Visa & Mastercard. The gap was larger in 2013 with American Express accepted at 2.4 million fewer locations. Traditionally American Express has been able to charge merchants higher fees than Visa & Mastercard due to their cardholder base being more affluent than their rivals. This is largely no longer the case with the introduction of other premium cards such as the Chase Sapphire Reserve and American Express also entering the other end of the market with the Amex Everyday cards. American Express plan to lower the discount rate by 5 to 6 basis points this year, typically American Express has been reducing this by 1 to 3 basis points per year.

{kind=link}

I preferred American Express’ previous plan of running promotions such as Small Business Saturday to try and increase card acceptance as it more directly benefited cardholders.

Hat tip to DrGForce & Financial Times

View Comments (19)

Amex is stubborn. If they weren’t so stubborn, they would have lowered their merchant fees 20 years ago to match those of Visa and MasterCard.

It is interesting to read all this Fees changes.

I've live in (mostly Hispanic) areas where they all taken Amex cards but they pass the fee to the buyers, yes a surcharge fee.

I really don't mind paying for the fee since the rewards I'm getting are much better (and higher) than those charges.

As long as, I get those rewards, the merchants (are happy) to help me meet requirements, and I can get protected for the items/services I buy, surcharges of $.30 or $.50 are meaningless to me.

What is not mentioned here is that (depending on a merchant's card processor) premium cards like Visa Signature and Infinite usually charge a higher fee than non-premium cards. I presume Amex is aiming to be closer to this range. I've even seen the rare food court merchant that had a small surcharge for rewards cards.

Only benefiting cardholder is simply the worst way to stay competitive...

They should just send people into stores with full baskets who pull out Amex cards and, when they discover they don’t take Amex, walk out of the store empty-handed.

Usually places that don't accept Amex are places that don't have a lot of high price items. Only place I have seen are small mom and pop restaurants.

My mechanic went from not accepting Amex to accepting it to not accepting it again. They started accepting it when the rates went down, but when a customer challenged a $5000 payment and Amex took the customer's side despite no validity to his complaint, they dropped it.

I hope AMEX doesn't reduce cardholder benefits to compensate for reduced earnings...

"Free Markets" are hard

The funny thing is that Visa Infinite (so CSR) has a larger interchange fee than that of AmEx cards. AmEx probably needs to create tiers like Visa and MC to keep profitability in exchange for more benefits.

Infinite and Signature are in the same interchange tier (for now), and they are lower than the published Amex fees no matter the category or card present v CNP

amex has different interchange programs too, such as one for its plat card with higher rates

you should compare apple to apple

This is not accurate. Amex charges the same rate regardless of card. MCC is Amex’s sole determining rate factor.

I only derived this from interchange+ payment processors' fees. All I know charge the same for all AMEX cards.

here are some AMEX IC (at least good till mid of 2017)

Retail 2.89% 0.10

Mail Order/Internet 3.50% 0.00

Restaurants 3.50% 0.05

Progressive insurance not accepting Amex was tough on me for a long time.

(Recently they added Paypal as a payment method so finally I can pay with Amex).

Change insurance companies. I just checked and Progressive was 300 dollars more than my insurance carrier per 6 months and my company accepts Amex for payment.

didn't think about using paypal as a middleman...thanks!

Thanks for the tip!.. Thought I was stuck using visa/MC too