Deal has ended, view more credit card bonuses by clicking here.

The Offer

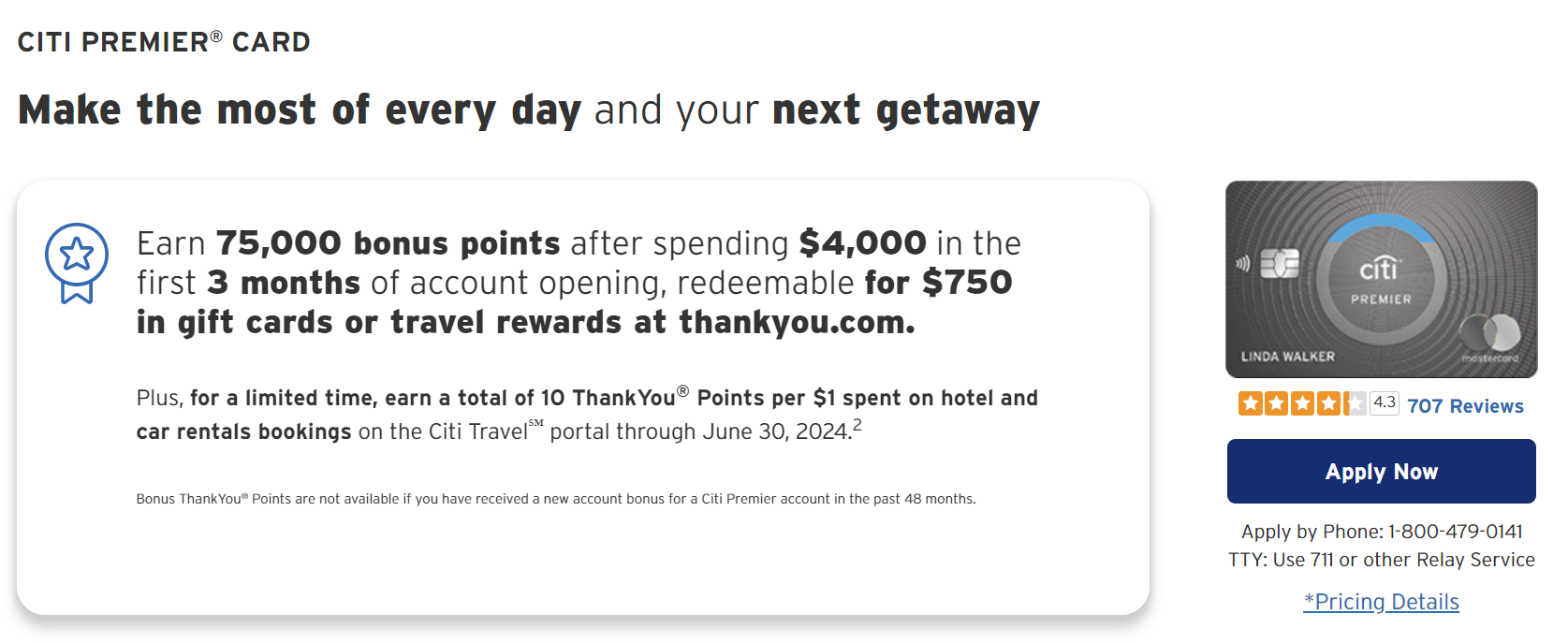

- Signup for the Citi Premier card and get 75,000 ThankYou points as a bonus after you spend $4,000 within the first three months.

- $95 annual fee is not waived the first year.

{kind=link}

Card Details

- Annual fee of $95, not waived the first year

- Card earns at the following rates:

- 3x Restaurants (including takeout)

- 3x Supermarkets

- 3x Gas Stations

- 3x Air Travel

- 3x Hotels

- 1x on all other purchases

- $100 off on a single hotel stay of $500 or more (excluding taxes and fees) once per calendar year through Thankyou.com

- Bonus ThankYou® Points are not available if you have received a new account bonus for a Citi Premier account in the past 48 months

Our Verdict

Not as good as the 80,000 point bonus that was available earlier in the year. As always make sure you read these things everybody should know about Citi credit cards before applying. We’ll add this to our list of the best credit card sign up bonuses. Some might prefer to wait for the Strata, but no gaurantee that card will ever launch.

View Comments (78)

Anyone been able to exchange your citi points for cash or statement credit? The citi premier card doesn't advertise it on the website but I heard that you can still do it anyway despite it not being advertised, trying to find someone who has tested this

I received a mailer this past week for the 75k for 4k spend within three months. It also includes 10x points on bookings through the citi travel portal through June 2024.

Would you please post a copy?

Weird. Got a very slow CSR that said I couldn't downgrade to custom cash. Will call again tomorrow for a better rep

I am interested in getting this Citi Premier with vested interest in knowing this possible policy change. Was it just an uninformed CSR or an unfavorable policy change in the making? Any feedback?

It happened to me also today. Did you by chance have any success to PC it to Custom Cash?

The 75K is definitely dead. It's 60K no matter how I open it as of today.

Same

Only showing 60,000 for me🙁 Anyone has a working link for 75,000?

Looks like the 75K points offer is no longer available now.

The link above showed the 75K offer for me, and I was just approved.

Same. Don't use the sponsored link from a Google search. Use this: https://www.citi.com/credit-cards/citi-premier-credit-card

Just heads up to others, that link shows 60K now as well.

Does Citi normally post new card sign up bonuses within a few days of meeting the spending requirement, or do they wait until the statement closes?

On 5/30, the deal may be over or changing as the website says: Earn bonus points after spending $ in the first months of account opening, redeemable for $ in gift cards or travel rewards at thankyou.com.

I saw the same thing and opened the page in a different browser. Got the offer to show up.

Approved with a $12k line. 0/6, 2/12 on TU, 800+, <1% utilization. I was worried about that low utilization, but I guess the low number of inquiries helped me out.

Approval Data Point (5/15/23)

Starting limit $2,000

At time of application:

Pulled 801 score from Experian (Pennsylvania)

New accounts: 3/6, 3/12, 8/24

Experian inquiries, 2/6, 2/12, 5/24

Income: $100K

Utilization: 3% of ~$200K credit (Within the last several months, utilization has ranged from 1% to 8%)

Citi relationship: Double Cash since 2016. No checking or savings ever.

I figured this would be a close one and the small starting limit mostly confirmed I was on the bubble to be approved. I have several other cards with limits in the $25K to $33K range.

Most of the data I saw were denials for those with 780+ FICO scores, at least 2/6 inquiries, and low utilization. I believe I got very lucky. Hope this data helps someone else.

Glad to earn that 75,000 Thank You Points though! Will wait 1 year and likely downgrade to Rewards+.

My application got turned down with a 820 FICO score and 0 late payments. They said I had too many credit cards with high credit and $0 balance.

I talked with a supervisor and asked why I was turned down. They said because of my credit report. I asked what the issue was with my credit report and all she could say is she could email a duplicate of the rejection letter I was sent. I asked "so you're saying I am a credit risk?". She didn't answer. I then said "all you have to do is say 'I am a credit risk' or that you are turning me down because you won't make money off of me and don't want to pay out the signup bonus even though you will make lots of money from the credit card discount fees you're charging the retail establishments where I use the card and I'll hang up". She replied 'I won't do that'. I mentioned to her that every time I log in to my Citi account I am prompted to get a Citi Premier card and I'm still receiving emails with a pre-authorized code to upgrade one of my existing Citi cards to a Premier card.

I get it, they're in the business to make money, but don't pee on my leg and tell me it's raining.

Last laugh, they sent my wife an invitation. We just activated her card.

I used to work in the "decisioning" for one of the big credit card issuers... so when I was there, they used the FICO credit scoring model, an internally developed credit scoring model and a PROFIT Model. When you talk to customer service, they pretty much follow a script and try not to deviate from it... so you won't really get a clear answer, but if you credit is very good, most likely your profit score is low. The flip side most issuers split folks into revolvers and transactors. Revolvers carry a balance, and usually have the crappy low rewards or no rewards cards (profit comes from interest), while transactors usually carry no balance, (profit comes from purchase volume based interchange revenue). So you would generate Pvol, which revenue that pays for the rewards programs typically, but if you just do the minimum spend, these profit models could theoretically capture that from your card balances on your credit report and generate a score and see you as a losing proposition as a churner.

Lol no me and p2 were/are carrying BT offers and that was their excuse to deny as we have too much credit utilized. Must be run by target lol