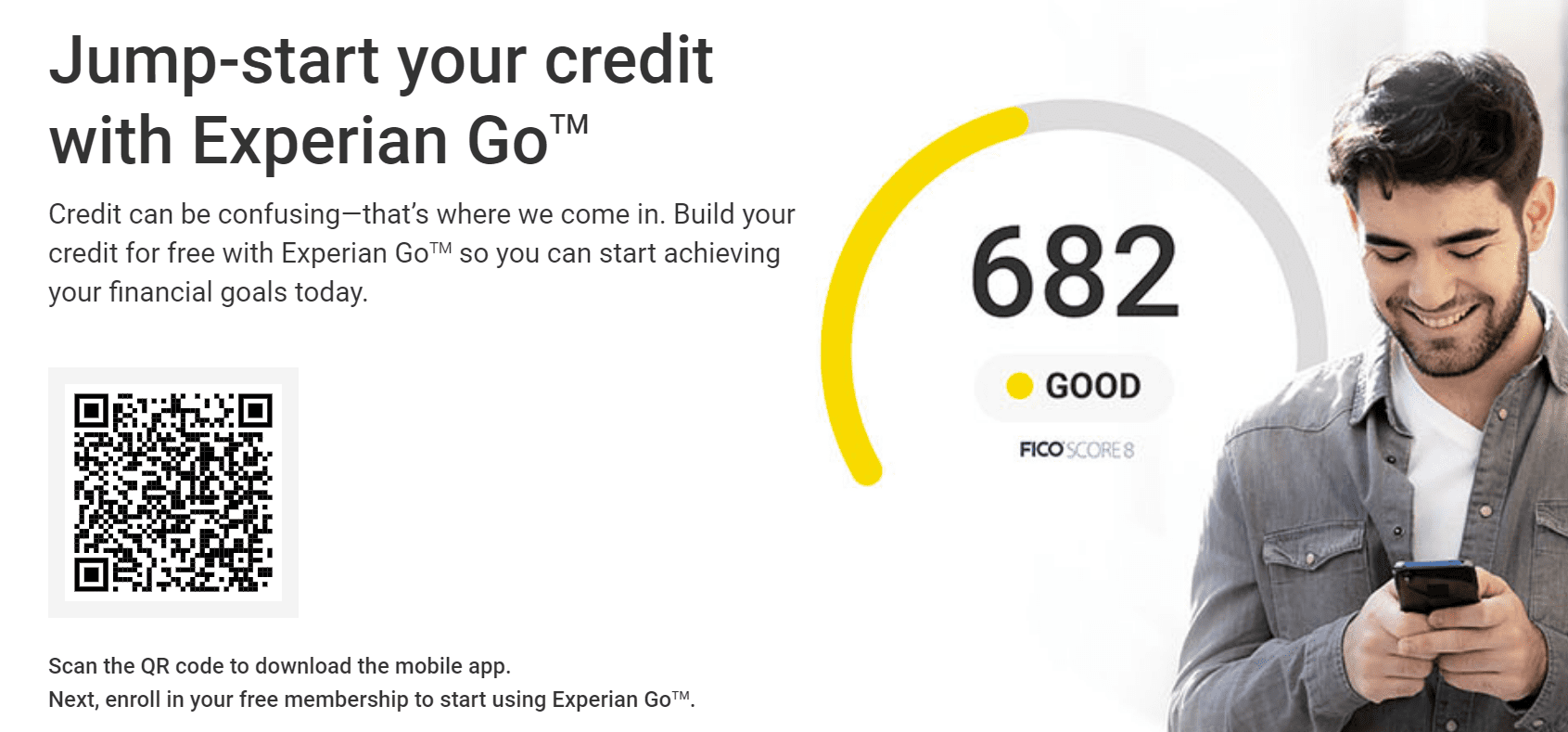

Experian has launched something called ‘Experian Go‘. The idea behind Experian Go is to allow consumers with little or no credit history to build their credit report. Once users sign up they have an authenticated credit report and can then use Experian Boost to add utility and telecom bills to their credit history. Experian Go also offers financial offers to users.

{kind=link}

This really just seems like a way of promoting Experian Boost and also pushing financial offers (presumably with affiliate links/partnerships).

View Comments (8)

I recently used over 50% of my credit limit for one of my low credit limit cards. My score unexpectedly tanked even though my total available credit of my entire portfolio is still very high. Can anyone provide any insight if credit bureaus weigh individual credit card usage more than total available credit used?

Does the boost business actually affect the credit score that lenders see, or is it just a feel-good number that you see when you log in to your Experian account? If it does boost your real score, how is that remotely ethical? They're presumably selling the additional info you're giving them.

I don't know much about it, but Experian's website sounds like it affects the FICO 8 score that lenders see (if they get that score from Experian). That doesn't sound unethical to me, since isn't that the reason that people would sign up for this?

But the whole point of the credit rating system is that it's a level playing field where everyone is evaluated according to the same set of factors, so lenders can make comparisons and know exactly what they're getting. If some people are allowed to get extra credit by doing favors to the credit rating company, doesn't that throw the whole system into doubt?

I guess it depends on what the contract between Experian and the lender says; if it doesn't specify exactly what factors are figured into the credit score, then Experian might not be violating anything. If the lender sees that scores from Experian aren't useful anymore, then the lender could stop buying scores from Experian (e.g., switch to a different credit bureau). Also, an article I saw says "some lenders exclude credit information from Experian Boost when evaluating credit applications".

Interesting. That disclaimer makes sense. So it really is just a feel-good score in at least some cases.

"This really just seems like a way of promoting Experian Go" - I assume you actually mean "Experian Boost" here.

Fixed