Update (11/21/17): As pointed out by readers Dan & Jeff S Northpointe is no longer accepting new applications for this account. I got in contact with Bill Clancy (VP/Deposit Banking at Northpointe) asking if this was permanent and what would happen to existing account holders and he provided the following statement:

Yes, correct – our 5.00% APY Ultimate Checking has been closed to new account holders. This is a permanent decision.

There are no changes at this time to any existing Ultimate Checking accounts. As with any business and any product, we’re continually evaluating our products and services to ensure they continue to meet both the organization’s and its customers’ needs. Our Ultimate Checking falls into this process as do all our other products and services. If or when a change may occur, it will of course be done thoughtfully and with significant consideration for what’s best for the bank, its shareholders and its customers.

Northpointe still offer their UltimateSavings (1.12% APY) & Money Market (1.5% on balances $25,000-$1,000,000) accounts. If you’re in the market for a high interest savings account, we’d strongly recommend reading our dedicated post here.

Offer at a glance

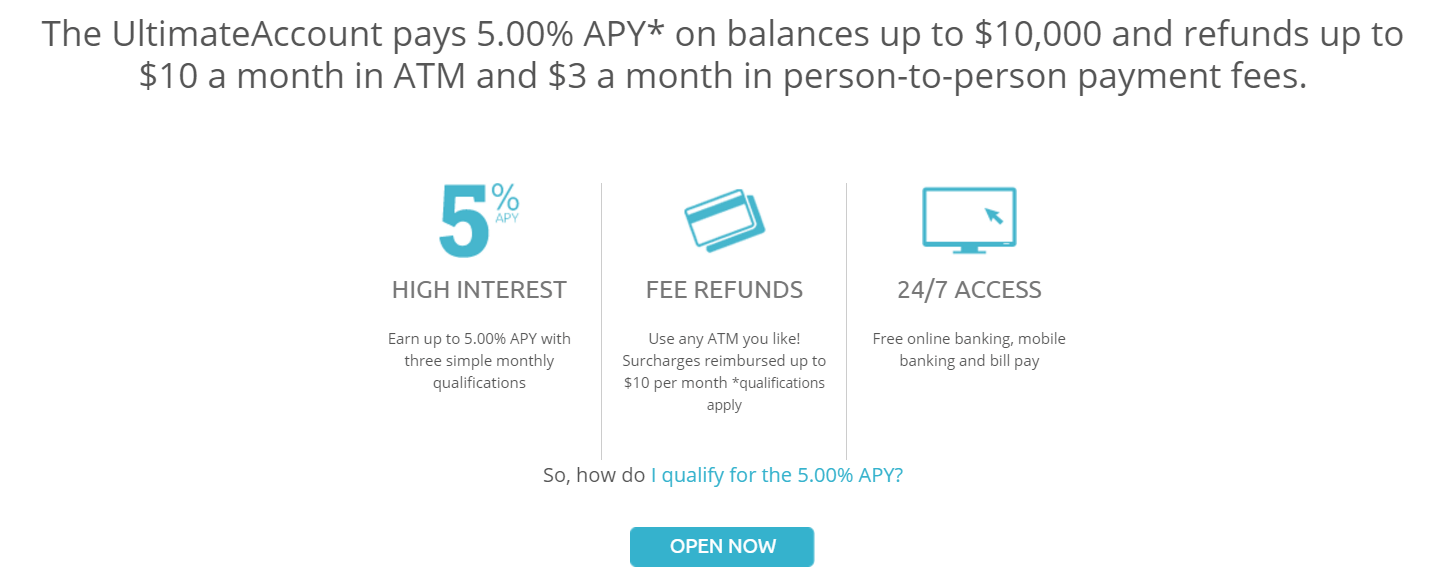

- Interest Rate: 5.00% APY

- Minimum Balance: none ($100 initial deposit)

- Maximum Balance: up to $10,000 (beyond that the rate is .10% APY)

- Availability: Nationwide

- Direct deposit required: No

- Additional requirements: Yes, see below

- Hard/soft pull: Soft

- Credit card funding: Yes, up to $100

- Monthly fees: None

- Household limit: None (one per SSN/ITIN)

- Insured: FDIC

Contents

The Offer

- Open the UltimateAccount checking account at Northpointe Bank and receive an interest rate of 5% APY on balances up to $10,000.

Any portion of the balance which is above $10,000 will earn an interest rate of .10%. (The first $10,000 will still earn the full 5% interest.)

{kind=link}

Requirements

There are three requirements necessary in order to be eligible for the 5% interest rate:

- Must enroll in e-statements.

- Must make 15 debit card purchases. (The 15 transactions must post and settle during the statement period to qualify.) More details on this below.

- Must set up an automatic withdrawal or direct deposit of $100 each month.

These requirements must be met based on the statement period, not based on the calendar month. If you don’t meet these three qualifications, then the interest rate is just .05%.

Meeting the Debit Card Requirement

Initially, this account had a 15 transaction + $500 debit requirement; since May 2017, the $500 requirement has been removed and you just need to hit 15 debit purchases of any amount.

That said, Northpointe has added terms indicating that they’ll switch or close any account that isn’t using the debit card in an ordinary manner for things like gas, groceries, and similar. We wrote more about this in a dedicated post.

Meeting the Deposit/Withdrawal Requirement

The direct deposit requirement is pretty typical, but here they gave us more leeway and allowed an automatic withdrawal as well. The main goal here, apparently, is that you should actually use the account and not just park $5000 in it, so they’re okay as long as they see some regular account activity such as a direct deposit or automatic withdrawal of $100.

Based on my correspondence with the bank:

- The $100 withdrawal requirement can be fulfilled, for example, by making a $100 credit card payment, initiated by the credit card.

- Making ACH transfers from another bank account may work in many cases to fulfill the requirement of a direct deposit, but it can vary by the bank as to whether it gets coded as a direct deposit.

Making an ACH withdrawal should probably work in any case since that doesn’t require a special ‘direct deposit’ coding to qualify. Thus, it should work for you to just have an automatic transfer of $100 from your regular checking account to your Northpointe account and another transfer back. Even if the transfer to the Northpointe account would not come up as a ‘direct deposit’, the subsequent withdrawal should presumably be considered an automatic withdrawal and suffice to make you eligible for the 5% interest rate.

Signup Bonus

There isn’t any signup bonus on this account.

At one point there was a $50 or $100 signup bonus offer, but it’s unlikely that will come back. At another point there was a $25 referral bonus offer which gives each party a $25 referral; also unlikely to come back.

The Fine Print

- Rates are subject to change after the account is open.

Funding the Account

The bank requires an initial funding of at least $100. The funding can be done via ACH transfer from your existing checking or savings account or via a credit card.

Avoiding Fees

This checking account does not come with any monthly fees.

The only fee to be aware of is a 12-month dormancy fee of $5 (more details here). If you are using the account for the 5% interest, this won’t apply to you as you’ll have activity when meeting the other criteria, but it’s worth keeping in mind. There is also an early account termination fee of $10 if closed within 120 days.

ATM Fee Waiver

Not only is the account fee-free, they’ll actually reimburse you for up to $10 in ATM fees charged by the ATM owner. (Northpointe themselves will never charge you any ATM fees from their end.)

This is a really nice benefit of having this account as you can always fall back on it to withdraw money at any ATM nationwide (or even internationally, perhaps) and get the fees reimbursed. Since you’ll already have $5000 in the account, you won’t have to worry about making sure the account has funds which you can withdraw.

Our Verdict

Since the account requires ‘ordinary’ debit card usage, it’s not nearly as valuable as a straight 5% APY account. That said, 5% on $10,000 is from the best high-yield options around, and some people will find it worthwhile to use their debit card regularly so as to get the rate.

Check our post on Best High Interest Savings Accounts for other high-yield options.

View Comments (395)

Don't forget to close your accounts out, guys.

just found out about this. i didn't receive any notice in the mail or email but after reviewing my past few statements, it looks like they switched mine in Nov 2017. had $10k thinking it was making 5% but it was only making 0.05% wtf. very frustrating. now i need to find a new place to stash my $$.

3/1 interest changing to 1%

Just got a letter saying the account is losing its high interest rate for existing account holders as well. Beginning March 1, the APY will lower to 1%.

So I guess we get to enjoy 1 more month of the 5% ... Ughh ... Open to suggestions ! That will probably sting a little come March 1st when everyone withdraws their money don't ya think?

KCCU offers a 4% and a 4.25% on balances up to $7,500.. Not Great, but better than nothing else.. It's a new offering as of December.. Makes me wonder if their 4% account on $15K is going away soon as well. (With the new offering and all) I might just drop mine in chance to get a $500 promo and then just go blow the $15K on something fun!

What $500 promo are you talking about Tim?

I just visited their website and I don't see anything even close to 4%.

As with all of these types of account there are typically limitations for most people. They are pretty open to the "doing business around the area" I do some contract work in West MI. I'm a CA resident. Just worked out. I can park 22.5K there at 4 - 4.25% worth looking into options.

There are a couple KCCU's and I finally found the right one Tim was referring to at Kellogg Community Credit Union (I believe). Unfortunately for most of us, you have to live, work, worship or attend school in a couple counties in Michigan to become a member.

Good information. I guess I could say I worship there? Nah ... not worth the hassle.

Or maybe we could get Tim to adopt us since being a relative to a current member gives eligibility also.

I got a letter today from Northpointe. They are changing the APY down to 1%. Also, you must accomplish $1,000 or more in debit card activity. Changes are effective 3/1/18.

Good while it lasted...

Any suggestion to move the money to different account or bank for similar or better interest? I already have insight/mango/lmcu. Even though interest rates are getting higher, it's getting harder to find bank who can pay us above 4%.

Also, how do I move the entire $10,000 from Northpointe to somewhere else?

Interested in replies to this as well. Sam ... I have considered trying insight / mango as well but I've been hesitant. Would you recommend then? I guess we'll all get 1 more month at Northpointe and then they will see a huge amount of withdrawals ! I'm interested in whatever information you can provide regarding insight / mango. thanks

William, It is 6 pages in all, but here are the 2 most important pages:

https://imgur.com/SFgTAl8

https://imgur.com/Da56zx9

If you need the rest, let me know. It's a lot of privacy policy stuff.

Thanks for the heads up Steve. On to the next one on March.

Thanks

Got a scan of the letter?

I've had this account for about 6 months but this is my first month actually trying to meet the requirements. I've used my debit card 15 times and they've all posted but the interest rate still says 0.05%. I noticed that some of the transactions say "CHK PURCH SIG" and others say "CHK PURCH PIN", obviously differentiating between transactions where I just signed and those where I used a PIN. Does it matter which type of transactions you make during the month? Confused why my interest rate is still showing 0.05%.

Does Northpointe support ACH pull for funding or is it push only? Couldn't find pull anywhere on the web site.

what you guys do to make those transactions each month? 15 seems quite alot to me, how about if i spend about 50$ on bjs but instead of paying total 50 i break it up in 10 15 and 25 for example, will they find that suspicious and not give me the bonus if they see 3 transaction from same place same day? also, any purchase will do the trick no? no matter if pin based or not, right?

If you don't already have the account open, this deal is dead for now anyway.

I pay my water bill, phone bill, trash bill, and internet, each twice per month. $3 -$5 each. That's 8 transactions right there. The rest is pretty easy.

I have made 2 purchases at the same merchant, in the same day, but they were hours apart. I wouldn't try several transactions at the same merchant, at the same time, that would be risky.

i do have the account and you my friend just gave me a hell of advise thank you very much, now i know how to make 15 transactions each month, and here i was about to close it, lucky i came here, hopefully they wont break the deal for existing costumers.

Could I make the humble request that you STOP making a whole bunch of transactions of just a couple bucks each month, you start making at least a couple larger ones too? It's clear that Northpointe is evaluating whether they will continue this for existing account holders (like me), and I'm sure a big factor in the decision is how many people do things like you do.

This is a "tragedy of the commons"/"prisoners dilemma" type of situation: we all share a common good, availability of this rate, and we might all be able to keep it indefinitely if few or none of us exploit it too blatently. But if enough of us try to take something that is a good thing even if we spend a few hundred on debit transactions, and try to squeeze just a little bit more advantage out of it, then it will destroy the benefits for all.

Please consider at least trying to make such a longer-term bet. At lest try to do it a few months. The deal is closed to new people now, so the existing population's behaviour may decide the fate of this deal, its in our collective hands.

Not sure who you're replying to, Mark. It seems like you're replying to me, although I don't make "a whole bunch of transactions of just a couple bucks". In fact I have never had a transaction here of "a couple bucks".

Bill Clancy has said several times, that 15x$1 transactions will most likely kill this. I make 6-8 at $3-$5, and the rest at higher amounts. If I had to make them all over $10, this deal then becomes too much hassle.

If you were replying to someone else, please accept my apologies.

You're welcome, glad I could help. I do the same with my CCU debit card. Whatever balance is left on those bills goes on my CCU credit card. 27 transactions per month between the 2 accounts.

Can somone explain to me how the 5% is applied? Got a lower interest payment than I was expecting despite meeting the requirements (although what I was paid out was greater than the default, 0.05% rate) and don't understand how it was calculated. Is the interest payment 5% of your ending balance at the close of the statement? 5% of your average balance for the statement? 5% of the daily balance compounded daily AFTER the requirements are met? The latter seems like it may have been the case for me. If that's so, this isn't nearly as useful as I thought it'd be as it took me half the month to accumulate enough transactions. Any help insight would be appreciated. Thanks!

Have you already done the $100 ACH deposit this month?

If all requirements were met and posted (not pending), your interest rate should show up as ~4.8% within a day and will apply to the whole balance at the end of the month.

Yep, I also met that requirement. Last month it showed up in the account online as 4.8888% once met, but the actual interest payment at the end of the statement was only about 65% of ((ending balance) * (0.0488888/12)).

Did you have the $10k for the whole month? I have never really done the exact math, but my interest is $38-$42 every month, which is more or less $500 a year. The only exception was the first month, because I funded the account in the middle of the month.

No, I did not have $10k in there the whole month. For about half the month the balance was pretty low as I was getting everything setup. I think that was the issue. I'll let it play out this month and see what the interest payment comes in at. Thanks for your helpful info!

sad day but can't say I'm surprised.

there was absolutely no way this was profitable for them especially with the DoC readerbase...

glad I held off though as I get more than my fair share of dealing with deposit accounts and banks as is