Deal has ended, view more Safeway deals by clicking here.

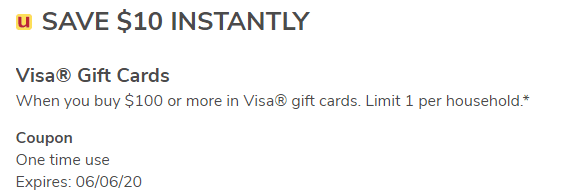

The Offer

Direct Link to offer (login required; filter by ‘gift cards’)

Check your Safeway Just4U for a digital coupon to get:

- $10 off instantly when you buy $100 ore more in Visa gift cards.

The Safeway deals are usually at Von’s, Albertson’s, Randall’s, Tom Thumb, Acme, Shaw’s, and Jewel too.

{kind=link}

The Fine Print

- Limit 1

- Valid through June 6th, 2020

Our Verdict

You don’t get fuel points on these Visa gift card purchases. Remember to save the offer before you use it, often the offer will disappear before the end date as well. Make sure to use a card that earns at a high rate on grocery store purchases or use Chase Freedom this quarter or any other card that’s running a bonus on grocery stores now. Normally these work on variable loads, but wait for confirmation in the comments if you don’t want to risk it yourself.

Hat tip to reader Roman M

View Comments (77)

This offer isn't available online or on the app anymore!

Mine is gone - from my saved list - I had it in 4 accounts, used from 2, but the second 2 I was saving until after a closing date. They are not there, I've checked twice. Double-check your account before trying to use!!!!

I SAY that, but maybe I didn't load it in all accounts last week...my memory could be wrong.

Just used the offer on my second household account, so there should be no problem with the offer staying on your card as long as you load it when it comes out.

Still have added to my account. Remember to save the offer before you use it, often the offer will disappear before the end date as well.

Not "often" but pretty much always. This offer disappears from Just4U about about a week before its expiration date.

loaded this to my safeway card, then tried to buy a 500 variable VGC today and pay with CSR for 5x bonus, but was told by cashier (and confirmed by manager) that they could only sell if i paid via debit or pin transaction on CSR that coded as cash advance. anyone else getting this or just my store?

go to another store

DP: The coupon worked fine on a non-kevlar Metabank variable at my Vons in SoCal. Posted as purchase on my Freedom ;)

I'm new to visa gift cards so wasn't aware there would be a $5 - 6 activation fee. Decided it wasn't worth it for me at that point

Yes, but it was still a MM, particularly if using a credit card that gives 5-6% back on supermarket purchases.

I have the coupon saved - however, when I tried to purchase a variable (kevlar) this afternoon, the coupon did not come off. It was with the usual guy I purchase with at the customer service desk, so I don't know if it's just that particular packaging. Anyone else have any issues today?

not today, but during a similar promo months ago. the rep just manually gave me a discount.

Same issue. Worked on another packaging (from Sunrise Bank).

Get this with the CashApp boost, 10% back up to $7.50. Comes to $88.45, or 11.55% discount, better than the 5% Chase gives you, especially if you are one to use points for cash back.

@guest_985895 Good tip! I had to reverse your values (backwards math) to determine how you arrived at 11.55%, but I finally got there. $100 Visa purchased with CashApp, then combined with the $10 (10% in this case) JusForYou coupon. Pretty awesome! My aim is typically $500 GC denoms. If I do a CashApp $100 and a $400 combo with my 7% CB grocery card, that will place my effective CB at 19.56%. Doesn't get much better than this by a long shot.

I just did the purchase a few hours ago. A couple weeks ago it was the Mastercard cards with the $10 discount. VISA or MC, same card in my book. Some dope on Slickdeals was all boasting about how he makes a full $500 purchase with the card with his 5% cash back on Chase Freedom (as opposed to the minimum $100). I mean, yeah, manufactured point spending since you are getting the card fee-free, but it is all about how you use points. If you are someone who uses points purely for statement credit (like myself), buying $500 is stupid, especially when compared to using the CashApp boost. I don't need to manufacture points to pay off credit balance when I can keep that $500 in my bank account. CashApp boost makes a $100 card worth $88.45, whereas 5% cash back Chase makes it $91.15. Technically the best CashApp rate would be at $75 (since the max boost is $7.50) but you need to get at least $100 to get the $10 discount from the Safeway deal. Now, if you are someone who uses manufactured spending to transfer points to travel systems, then things become markedly more complicated. Some of these guys have the Chase Sapphire Preferred card. You can link your Chase Freedom Ultimate Rewards account and transfer points 1:1 for free, at which point the points become worth upwards of 1.5 cents per point (vs the 1 cent/point for statement credit) at certain travel partners.

A couple examples from ThePointsGuy commenters:

1 - 118,000 points for a flight from LAX to Singapore on Singapore Airlines in first clast, which would have cost $8500. Approximately 7.2 cents per point.

2 - 100,000 points for 4 tickets from LAX to HNL, approximately $700 per ticket, so around $2800 total. Approximately 2.8 cents per point.

I've read that you get MUCH better value for your points when you redeem for business or first class travel, thus the marked difference.

At 2.8 cents per point, it would be like getting that $100 gift card for $82.51.

At 7.2 cents per point, it would be like getting that $100 gift card for $61.39.

Sound like great deals, but you gotta be a traveler (especially at the high end) to really get those values. If you aren't a traveler, stick to CashApp boost...lol.

@guest_985895 Wow... that's enlightening. I didn't know the Chase rewards structure operated that way. I'm not big into the Chase ecosystem however as I have a general disdain for them being a large bank (not to mention they renege on their points if they cut you off for MS, lol). However, given the factual scenario points you provided, how much reward earnings using the 7.2 percent setup would it take to offset the massive annual fee on the CSP or CSR?

In the 7.25 cents per point example, category spend at 5% initial cash back would be achieved at spend of $16,275.86 to yield $8,500 point conversion (118000 * 7.25 = $8555; $16,275.86 * .0725 = $1179.99) in rewards redemption? That's still only 7.25% against a higher spend threshold vs the lower spend allowance (preference in my case using CashApp). Yet and still, a 16K spend is a bit much for me--serious overkill actually, lol.

To get a $38.61 in return off that $100 GC would not cost $61.39 factoring in the coupon and 7.25 rewards redemption, unless I'm missing something here. It would only yield a 17.25% savings.

Honestly, what it comes down to is how you value your time. These guys who are manufacturing spending on their Chase Freedom card and Chase Sapphire Reserve card need to spend inordinate amounts of time trying to figure out how to liquidate those Visa/MC prepaid cards. My wife's friend's husband is a big time manufactured-spending churner. He always does the Visa/MC prepaid card deals when there are deals on the cards. In his case, either he takes the cards to gas stations and pays for peoples gas while receiving cash, or he does money orders at Walmart in some fashion. It takes a lot of time but it works. They, as a couple, have gone on a lot of extravagant trips in the past several years - Italy, China, Thailand, etc. They save 100% on airfare.

My math for the $61.39 is as follows:

The purchase is $100 + $5.95 - $10, or $95.95. Putting the purchase on the Chase Freedom at 5% bonus, or 479.75 points. Transferred to Chase Sapphire Reserve it is 479.75 points. That 118,000 pt Singapore ticket (valued at $8500) relates to $0.072 per point, or 13.88 points per dollar. If you assume that all those Chase points will be redeemed at 13.88 points per dollar whenever you buy tickets, then those 479.75 points have a "value" of $34.56. So whereas a statement credit of $95.95 yields $4.80 in 5% statement credit value (i.e. a final cost of $91.15, $95.95 - $4.80 = $91.15), that $95.95 yields $34.56 in travel "value". $95.95 - $34.56 = $61.39. It seems kinda strange to have such a high exchange value, but the catch is that you won't see that actual $34.56 value until you get up to 118,000 to be able to redeem it. You can't redeem 480 points for $34.56 towards an $8500 ticket.

The question at that point becomes this... So assuming you are accumulating 118,000 points in spending without the initial bonus perks for Chase Freedom (20000 points after spending $500 in 3 months) or for Chase Sapphire (50000 points after spending $4000 in 3 months), that is $112,000 in spending to get those 118,000 points (110,500 at 1x, $1500 in Q2 limit for 7500 points), could you do better investing the money you take as statement credit over time? I split up my spending on different carts to maximize cash back value - 4% Capital One Savor for dining, 3% groceries on AMEX (when not using Chase Freedom), 3% for online shopping on BOA, 2% wholesale on BOA (when not using Chase Freedom), and my gas I get creative since my BOA card is always set to online shopping (I use Chase Freedom in Q1 and Q3 every year, in Q2 and Q4 I get Shell gift cards from Best Buy using their credit card, which gets me 5% in store). I'd say I average around 2.7% cash back when everything works itself out. $112,000 (which, by the way, would take me over 6 years to achieve) * 2.7% = $3,024. I think I can use that $3,024 in the stock market over 6 years and get a better return than $5,476. Oh and by the way, I wouldn't buy a first class ticket ever, so the Hawaii example is more relevant to me (2.7 cents per point is no better than what I get with my spread out spending).

Trust me I get the allure of being able to get some free tickets. But it is too much work to manufacture spending. I have a hard enough time as it is convincing my wife to buy in on some of these deals.

Side note: I always put my airfare on the Orbitz credit card. That gets me 6% (!!!) cash back on Airline purchases (and 10% on hotel purchases). Now, the catch is that the money is stored as Orbitz cash, only good towards hotel purchases. But I get a lot of free hotel nights as a result.

ah there is always the argument that you could do both - invest as well as manufacture spend. There is a learning curve to MS, but once you master it probably becomes second nature.

Also, its treated as a hobby or a game by most - not just a financial savings tool by itself. So you got to think that these people are enjoying the MS portion of it as much as their travel portion.

I don't do as much MS as your friends but when I see a deal I can easily make use of I just get it without having to go out of the way. For instance if I was in the store to buy groceries why not get the GC?

[Signs up for Orbit CC while typing this response... =).] You definitely have a point there on the collasel effects it would have to take using those MS techniques to rack up mileage rewards to cover airfare in the Chase portal. My essential expenses for 6-yrs wouldn't even amount to 112K spend. That's bonkers for my situation but if it works for others then great for them.

Like you, I would much rather generate dividends from stock and higher earning CC offers and bank SUBS vs playing the Chase premium CC game. The goal is usually 7-10% or greater. My Affinity CC offers 7% on grocery and gas till the end of the quarter (Q2). Amex BCP as you know is 6% all around for groceries. Plus DiscoverIt (10% year 1), Chase Freedom (5%), and Nusenda (6% CB during cat period--this is often misreported as only 5%) offer hefty grocery CB also. This setup fits my pocketbook much better, keeping the spend lower and rewards heftier, particularly when a GC coupon is involved.

As for the wife friends hubby, he has guts to be able to solicit others to convince them to fork over their cash for his GC equivalent, lol. If I didn't live in such a warm climate here in south Texas I'd probably try his approach as a last report.

In closing, who's to say one couldn't achieved a better deal by hunting around (finding a lower cost ticket outside of Chase portal, thus negating all the high spending which becomes useless)? I wish there were solid data points on this type of comparison/contrast. Who's really winning in the end? Hands down, Chase!!! At the end of the day you're still in one big tube called an aircraft en route to a dream destination... unless a pandemic interrupts that.

Same here! Got the groceries on the Hyatt card then put the $100 of the VGC entirely on Cash App.

Can you explain the math here? First time I'm hearing about CashApp boosts.

@Pablo CashBoost is a neat feature of CashApp. It takes revolving merchants ("Any Grocery Store", "Wal-Mart", "Taco Bell", "Chipotle", "Door Dash", "Walgreens", etc) - 8 in total - and offers you a savings rate of 10% (although in the past they have been as high as 15% during the holidays for some merchants). Current boost as of today: DoorDash, Shake Shack, Walmart, The Home Depot, Chick-fil-A, Playstation Network, Whataburger, & Xbox.

You must apply (guarantee approval it seems) for the card directly through CashApp itself (you'll receiving it in ~7 business days; it's a functioning debit card essentially; you can instantly load it from any checking accounting associated with a debit card). As of recent, you also get an acct & routing # for easy ACH transfers (although these take likely longer to post when pushing from an external bank). Debit transfers are usually instant.

You can attach/link multiple debit cards and or bank accounts to "Deposit the funds" pulled from said linked debit card--making money transfers seamless and quick, if you're like me and find that ACH is akin to USPS snail mail. Overall I find the process of transferring money from one of my accounts to another a lot less hassle using the CashApp method vs test deposits that other financials institutions employ, especially when it comes to small dollar amounts.

The catch: The max spend to receive the INSTANT 10% reward is $75. After that, 0% earnings using CashApp card. The plus side is that you can make as many trips to said merchant that you choose as long as the trips are spaced at least an hour apart. And you MUST reactive the boost every time between purchases of the selected merchant.

Strategy: Let's say there's a $300 item that you want from Best Buy. If you want 10% off this select merchant, you'd have to visit Walgreens/Grocery Store 4X to purchase one $75 gift card each visit. You effectively save $30 or 10% off the entire $300 spend by employing this technique.

The 10% boosts expires within a week and new boosts are created on Fridays at 11 AM CST or so to replace expiring boosts (there's a countdown in the app that reveals how many days/hours remain before the boost expires). Only one boost can be active at a time. Very important: Boosts can be recycled every 1-hour period. Boosts expire 10 AM EST (noon CST, I confirmed this with Cash App customer service); lesson learned: try not to wait till the last morning hours of the expiry day to use a boost).

I tried this but the grocery boost didn't reset after an hour. It seems that you can only use it once per week, not once per hour like you claim.

Nick, what he means is that if you are intending to use two boosts in succession, you need to space it out by at least an hour. The app makes available multiple boosts which you can enable in succession, but need to be spaced out. So if for example you were planning to use a boost at a grocery store and then go next door to walgreens to use the walgreens boost, you need to make sure you wait at least an hour after making the grocery purchase to make your purchase at Walgreens.

The boosts refresh every week.

Ive used safeway gift cards to buy VGC. Ive also used VGC to buy VGC (churnetting). It works here in hippy dippy nor cali. Never hurts to ask.

lmao @ hippy dippy hahaha

Can you please explain economics of buying VGC with VGC? How is it a money-maker?

Well, it's a $3.05 MM.

I guess @Robert has multiple Safeway/Vonns/etc. accounts.

#Guilty here. The "One Coupon Per Customer" restriction doesn't cut it for me; I have four of five Safeway account$. (The hard part is remembering what associated phone number I have used recently; this can be verified by logging into the account and if the "Just 4 U" deal is still viable within that login, then you're good to go. Otherwise, simply act as if you don't know why the app is "malfunctioning" and the cashier will call the manager to manually override--I have done this 2-3 times when the last Just4U offer was available in early March this year.)

Question: Does the $10 off apply to variable load Visa GC as well? Using my 7% grocery CB CC with this offer would net a savings of 6.19%; I'd likely touch on this once or twice if the $500 Visa GCs are a viable option (based on a below post I see that this is true). I will be taking advantage of this offer.

Correction: 7.81% is my net earnings using $500 GC as a baseline (sorry, I forgot the negative sign in my formula). The $10 coupon offsets the $5.95 activation fee yielding an .81% (4.05/5)profit. Add my 7% rewards card and that puts me over the hill at 7.81% in earnings. It's a great day! =)

When was the last time you used Safeway gift cards to purchase VGC? Also, did the cashier have to override anything or did you just proactively ask first?

With most folks feeling a bit more comfortable going into grocery stores, this deal will likely be quite popular -- especially with the generous short term bonuses being offered for grocery spend by some card issuers. For example, putting such spend on an AMEX Hilton Surpass card seems quite desirable, especially if you can hit $15K in annual spend for a free night anywhere,

Can confirm successfully works for variable load at Safeway.

Would be helpful to know where and what kind of card exactly.

Apologies for the ignorance, what do you mean by variable load? Does that mean it works for gift cards over $100, like a $200 gift card?

Scott referred to a variable load visa gift card (vs one with a fixed amount like $100 or $200) allows buyer to select the amount to be loaded into the card at purchase time. You can typically find ones with choices from $20 minimum to $500 maximum.

Is it possible to pay for the Visa card with a Safeway Gift Card?

Once upon a time, it was allowed in most stores. Then at some point a few years ago, Safeway corporate sent a memo that it was not allowed. However, they never reprogrammed the registers to disallow it. The first time I tried it after the memo went out, the cashier was unsure and called her manager. The manager allowed it but then got upset at the cashier for apparently not clearly explaining the transaction. So, since the manager said corporate doesn't allow it, I haven't done it since to avoid causing trouble for the cashiers. The policy is that you can only buy groceries and not purchase any gift card with a Safeway GC.

@guest_985811 Why would you do such a risk thing like that?

How is that risky?

I'm going to try and buy a VGC with my Safeway GC this week. The worst that could possibly happen is that it doesn't go through. Then I'd use a credit card.

let us know how it works. i have a safeway gc that i haven't used. this could be a good deal if you buy safeway gc at a discount, like during the amazon promos found on this site.

Ymmv, test & see... be own DP

Nope, unless you are a nephew of the cashier.