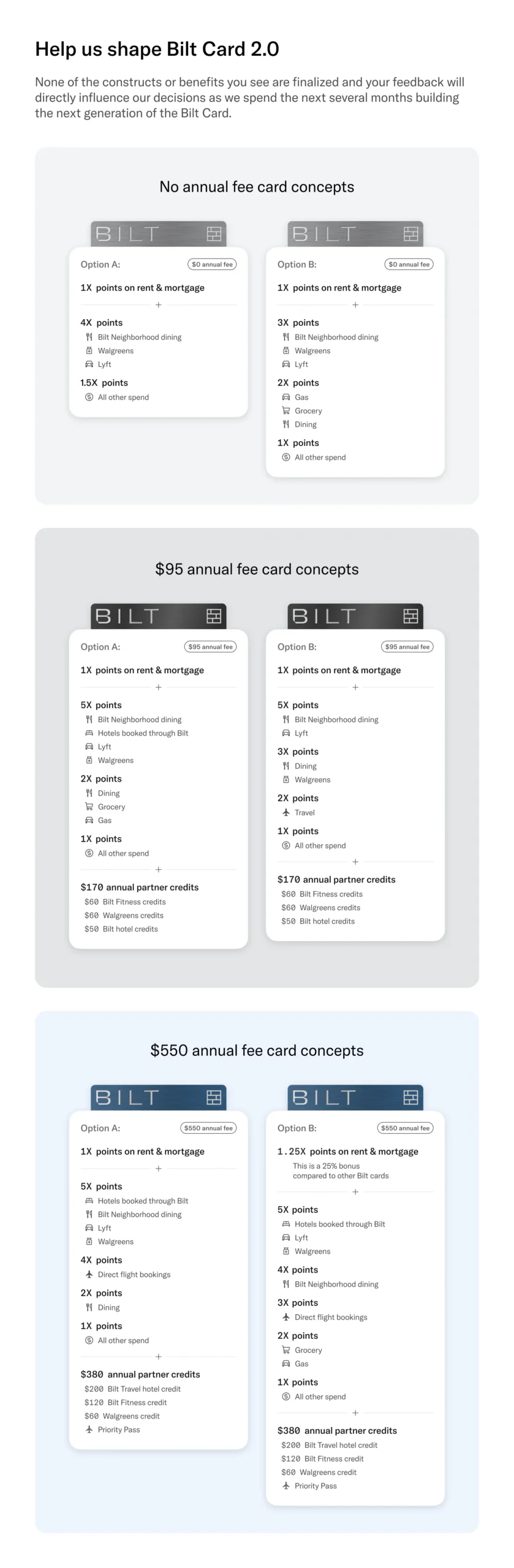

Bilt has communicated with existing customers regarding a Bilt 2.0 credit card. This was teased in the 2025 roadmap. Seems like there are three different tiers, no annual fee, $95 annual fee and $550 annual fee.

Bilt has communicated with existing customers regarding a Bilt 2.0 credit card. This was teased in the 2025 roadmap. Seems like there are three different tiers, no annual fee, $95 annual fee and $550 annual fee.