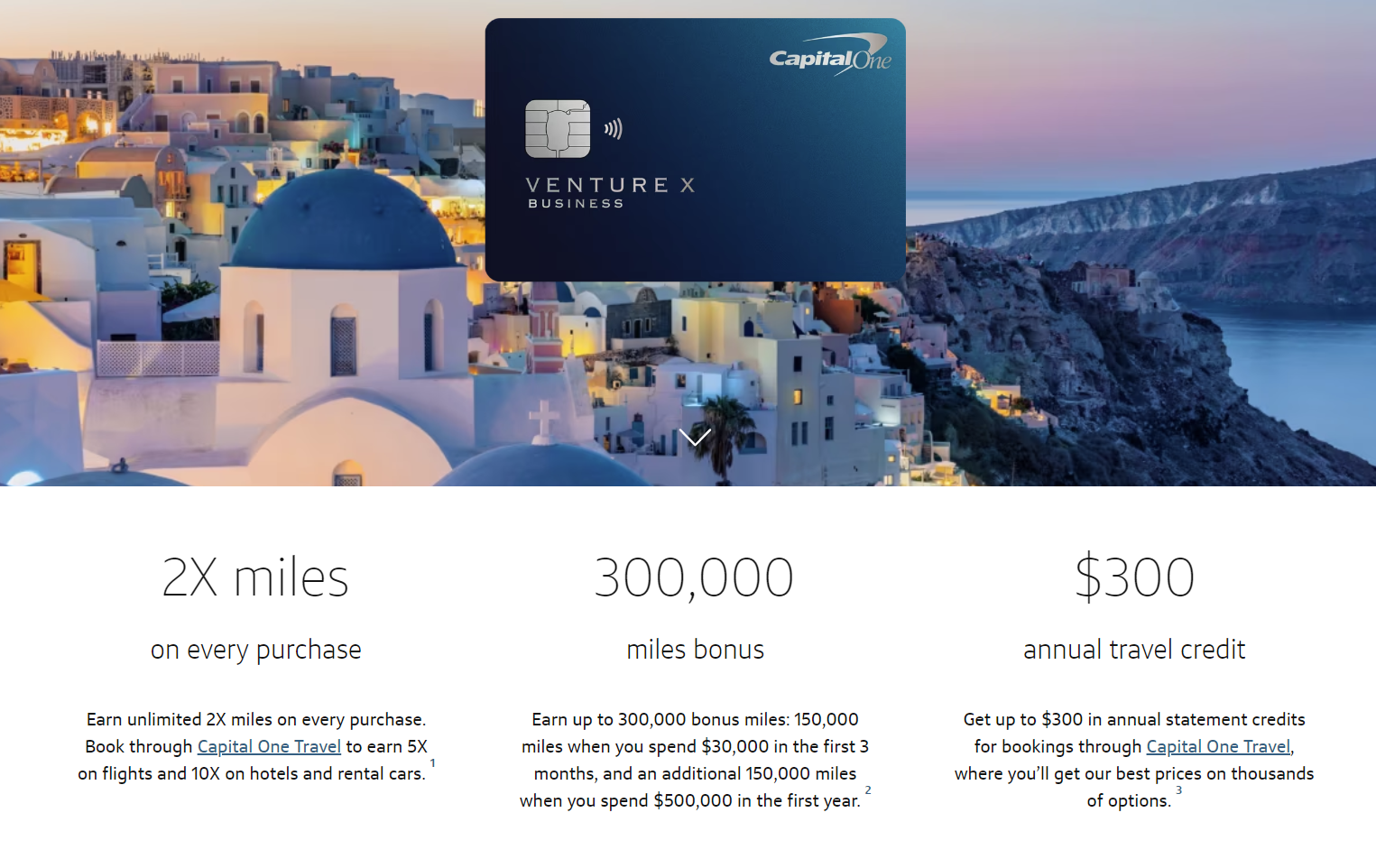

The Capital One Venture X Business card is around for almost a year, yet still requires applying directly through a business relationship manager. Interestingly, Reddit user fezud reports that they’ve changed the details of the signup bonus. Here is the new bonus offer:

- Earn up to 300,000 bonus miles: 150,000 miles when you spend $30,000 in the first 3 months and another 150,000 miles when you spend $500,000 in the first 12 months.

- Previously the signup bonus was a bit lower at 250,000 points, but had a spend requirement of ‘just’ $50,000.

$500,000 is the highest spend I’ve ever heard of, insane! It’s not even a great bonus for that amount of spend. I suppose that someone who anyway spends a ton on their card might find this bonus interesting since the card has a nice regular earn rate of 2x per dollar as well.