The Cascade card is a new prepaid card that lets you earn up to 100% (or more) cash back on non-PIN transactions. You know the saying “if something seems to be good to be true, it probably is?” Let’s see if we can’t prove that saying right.

Contents

The Basics

Before we delve too far, let’s try to understand the basics of this card. For me the biggest is that the card actually isn’t available yet. If you go to “get your card” you can reserve a card.

- You must spend at least $350 per month in non-PIN transactions to receive cash back

- Account is FDIC insured

- No credit check involved

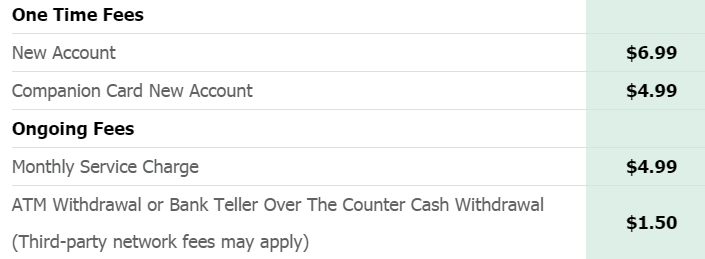

- New account fee of $6.99

- Monthly fee of $4.99

Fees

The Cascade card comes with the following fees:

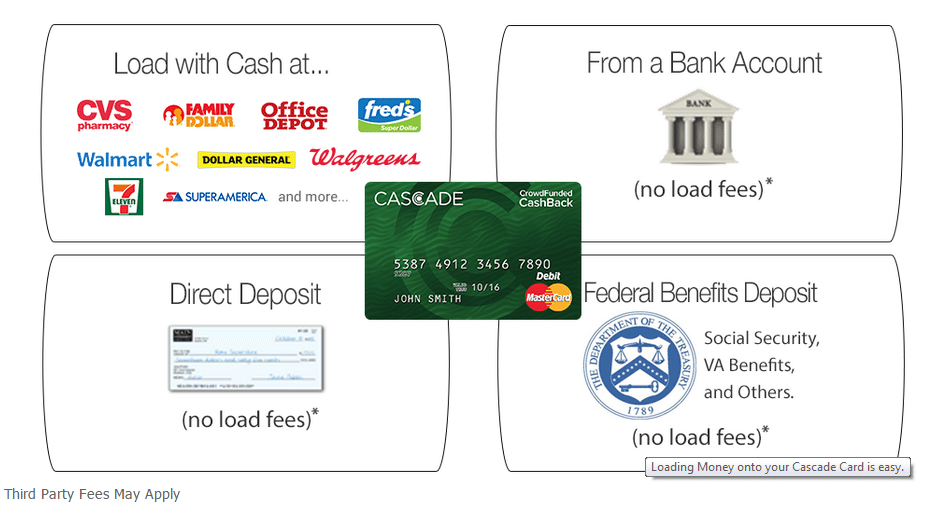

Loading The Account

You can load your Cascade card with the following methods:

Earning Cash Back

Now the part everybody has been wanting for, how do I get 100% cash back on my non-PIN purchases!? You can watch this “informative” video from Cascade to get some idea of how the program works:

Basically you need to spend at least $350 per month on non-PIN transactions per month to be eligible for cash back. You’re not eligible for cash back until you’ve earned at least $350 per month for three consecutive months.

Every person you refer also becomes part of your CashBack Crowd, the people they refer also become part of your CashBack Crowd and so do the people they refer, this keeps going for a total of six levels deep. To simplify things, the more money your referrals (and their referrals) spend the more cash back you’ll eligible for.

It’s actually possible to earn more than 100% cash back by becoming a diamond member (more on this here).

You have to pay taxes

The F.A.Q states that you must pay taxes on your earnings and they’ll send out a 1099 form at the end of the tax year.

Our Verdict

This seems like a good old fashion pyramid scheme (although they say they aren’t, they also say they aren’t a MLM scheme), the more people you refer the more you receive. I’m sure they’ve structured the cash back in a way that they always turn a profit on the interchange fees. If you’re at the top of the pyramid and have a lot of referrals (and they refer a lot of people) I’m sure you can get some money out of this program, but in reality you’re really just taking money from your friends/referrals. Let me give an example:

- You refer three people and they all refer three people each, you’ll have the following amount of referrals in each tier:

- Tier One: 3

- Tier Two: 9

- Tier Three: 27

- Tier Four: 81

- Tier Five: 243

- Tier Six: 729

- That’s a total of 1,092 people spending $350 per month minimum, for a grand total of $382,200. If you put that spend on a 2% cash back card it would total $7,644. Instead you’d earn $343.98 or 98.28% cash back.

- Cascade will also earn $5,449.08 in monthly fees from your referrals

Now obviously this doesn’t take into account that people in tier two-five will also receive cash back from their referrals, but it also doesn’t take into account that some people will spend under $350 per month and thus not be considered an active referral and some people will spend well above $350 per month.

I’d recommend staying well away from this card, as always: if it’s too good to be true, it probably is! Am I missing anything? Let me know your thoughts below.

Hat tip to Maximizing Money

The card has gotten even better check it out @ http://www.cascadecard.com/keepmicro you can get paide regardless of the amount

You spend and avoid all fees. Free transfer fo funs friends to friends!

Frank FRANK

Hi Frank, what’s your association with the card? This comment reads like a paid ad.

Yes, I got a card a month ago. Firstly, when I got my welcome email, it contained the wrong person, Nicholus …… So I had access to his account or he had access to mine, or both. I thought this was a huge problem right off the black, but some guy named Spencer Schmerling charmed me into staying with the account, and I did. He said they were new, and I figured it was a simple mistake. But thinking back on that, it was my stupidity falling for his charm and sob story. Live and learn

I put 500 dollars on it and used the card online. The transaction went through, but but I didnt’ get credit for the non-pin transaction. I have an email from cascade card, admitting to their error. I made another 500 dollar purchase and it was fraud blocked by the merchant seller account. I made a 15 dollar purchase, and it too was fraud blocked, but it was the weekend. So I figured I’d fix it on tuesday business time, as Monday was Martin Luther King Jr day.

On Monday, Martin Luther King Jr day, I got an email stating my account was suspended for “suspicious activity.” I called them and Spencer Schmerling stated that my 1/2 a dozen 40 to 100 dollar deposits, “were overt signs of fraud!” He was accusing me of fraud, and suspending my account. I told him I thought that was absurd, and then my account was closed, so that I could not access it online.

Martin Luther King Day, I has having my civil rights violated by Sunrise Banks, and Cascadecard, not making me sit on the back of the bus, they they were stealing my money and taunting me over the fact I could do nothing about it. I’ve never been so humiliated.

I’ve spent the day filing complaints, and everybody is closed! So tomorrow and the next day and the day after that, I have to drop everything to get my money back, and warn other people, as a duty and obligation to society, that cascadecard is scammed me out of my hard earned money!

I think that if your claim were legitimate, at some point, you would have sought to access your money through your pin (ATM). The fact that this was never mentioned in your narrative makes me suspect that something is fishy in your story. I read what you said, but I wonder what you’re leaving out?

Mr. Picasso, why so bold to defend them using theories that most of the world understand are not cogent. Frozen accounts cannot be overcome by going to an “ATM” machine. Sunrise banks ruled in my favor, gave me back my money on Tuesday, and that was that! Why would anyone want to risk losing their paycheck

continuing my feedback:

“That’s a total of 1,092 people spending $350 per month minimum, for a grand total of $382,200. If you put that spend on a 2% cash back card it would total $7,644. Instead you’d earn $343.98 or 98.28% cash back.”

“If you put that spend on a 2% cash back card it would total $7,644.” true. if i bought $382,200 in one month on my 2% cash back card i’d get back $7,644 of my money. i don’t know that many people who put $382,200 per month on their credit card. do you? thus this line doesn’t belong here and should be deleted. because what i spend on my current cash back card can’t be compared to Cascade’s commission structure 6 levels deep!

“Instead you’d earn $343.98 or 98.28% cash back.” should read (with the prior sentence deleted): ‘With Cascade you’d earn $343.98 or 98.28% cash back.’

“Cascade will also earn $5,449.08 in monthly fees from your referrals” did you get that amount this way? $382,200 x .014257? i don’t remember reading that Cascade keeps 1.4257% of their interchange fees. i derived .014257 via: your $5,449.08 ÷ $382,200. where did you get the $5,449.08 or 1.4257%?

anyway, how much Cascade keeps of the fees they earn by processing $382,200 in charges is largely irrelevant for a prospective Cascade cardholder. they company will make what it makes. without Cascade sharing their interchange fees with the public they’d keep the full (2% +/-) amount. by opting to split their fees with the public with their 6-deep payout plan they should grow their processing business tremendously!

the article reads and my comments: “This seems like a good old fashion pyramid scheme (although they say they aren’t, they also say they aren’t a MLM scheme),” in a pyramid scheme the money paid in by new members is divided up to existing enrollees. here a new enrollee gets a card for $6.99 and none of that $6.99 is paid out upline. none of the $4.99/month is paid out either. in an MLM (which is a marketing method and not a scheme) you get a commission based on what your downline buys each month, and possibly also on your own purchases. my understanding of Cascade is that *your* monthly spending is not part of *your* commission. and you don’t earn on the stuff being bought by your downline, but instead earn based on the interchange fees generated by your downline. note that Cascade doesn’t use the upline/downline terms. MLM’s also sell products, and may require a minimum amount of their stuff to be bought each month. Cascade doesn’t sell products. “the more people you refer the more you receive. I’m sure they’ve structured the cash back in a way that they always turn a profit on the interchange fees.” of course! when they devised this plan i’m sure they *started with* how much of their interchange fees they could afford to relinquish to card referrals. just do the math based on their website. if they earn a 2% interchange fee per swipe, i think i read (or calculated) that they’re paying out .54% (.09% x 6 levels below you) and keeping the other 1.46%. so they’re splitting their interchange fees with the cardholders. which is 100% more than other credit/debit/prepaid card companies do! “If you’re at the top of the pyramid and have a lot of referrals (and they refer a lot of people) I’m sure you can get some money out of this program, but in reality you’re really just taking money from your friends/referrals.” a Cascade card holder is not taking ANY money from his/her friends/referrals! the bank/merchant processor/interchange companies are earning their (hidden to you) fees from the *merchants* who accept credit/debit/plastic. you go to the store today and buy $100 worth of stuff and pay with plastic, the store may wind up with, say, $98 in their account. many consumers aren’t aware that the seller doesn’t get 100 cents on the dollar when you use plastic! and if you don’t pay off your credit card charges in full each month then you’ll pay interest, also going to the bank. so the bank wins every time you use your card and will make money whether you pay your balance in full or not. when you use your plastic card those (hidden) fees charged to the merchant are not known to you, and *you* are not paying those fees, the merchant is. Cascade is sharing those interchange fees 6 levels deep. so a Cascade cardholder is NOT having any money being taken from him/her by his/her referrer… Read more »

Great insight Barry! Thanks for the comment.

Well said Barry

Permit me to address two issues. 1) the implications that Cascade Card company is “short changing” it’s customers by paying out comparatively miniscule earnings to them; and 2) the Ponzi Scheme idea. I am a Cascade cardholder; and my understanding is that there are at least four parties involved in this offer: 1) Sunrise Banks NA; 2) Mastercard International; 3) Merchant Services (the entity that collects the interchange fee from swipes); and 4) Cascade Financial Technology Corp. From my experience as a bank customer, there is absolutely no doubt in my mind that the biggest winners here are the banks and financial services corporation. Banks will not ever lose! In this equation, Cascade is the lowest on the totem pole, and is sharing its earnings for six generations of customers! Secondly, regarding the Ponzi Scheme idea, does anyone here think that Mastercard International will affix its name to anything that vaguely resembles a Ponzi Scheme? If indeed Cascade Card were running a Ponzi Scheme, does anyone think that Cascade would be daring enough to “sneak” Mastercard’s logo onto their card to give the appearance of legitimacy? And would Sunrise Banks go along with that? I would be careful about innuendos that seem to border on accusations.

Great points Princess

I have the card. Great customer suppor .

http://www.cascadecard.com/KeepMicro

Frank

This article is very misleading, It’s full of assumptions and wrong information.

And this is why I’m glad to have bloggers like you do a comprehensive analysis 🙂 I felt uncomfortable about it as soon as I read about the referral scheme. I always feel uncomfortable spamming people with referral links and only do it when it benefits both people significantly (without requiring extra work like needing to refer MORE people).

Ay caramba! This will not end well.

Fingers crossed it doesn’t end well for Cascade and not their cardholders.

Imagine the monthly disappointment you will go through as the referrals miss their monthly spending mark. You would not have any idea of whether or not the company was paying out accurately, and you would still have the fees. It sounds like a lot of work and faith in others to meet their marks, assuming the company accurately reports and tracks everything. How easy would it be for the company to misreport every month with no real consequences.

Like every good pyramid scheme, you must be at the top to reap the rewards.

A person in your CashBack Crowd does not have to meet any monthly threshold. Lets say I referred you and you only spend $100 on your card, I would still get Cash Back if I spent $350.

The company is sponsored by Sunrise Banks N.A. which is a Federally chartered bank. They audit the CrowdFunded CashBack program.