Update 4/19/21: Plastiq has confirmed in a statement that these changes have no effect on Plastiq payments, and that Plastiq does not process any payments which are cash advances so there’s no need to worry. They’ve also tested it out themselves and have not seen or heard of any cash advance issues.

We understand that Chase made an announcement a few months ago about cash-like transactions and third party payments, effective April 10. There was some concern that Plastiq’s transactions would be impacted. At the time of the announcement, we were assured by the card networks that Plastiq transactions would not be impacted by those changes and we communicated that to our customers who inquired. Transactions that would be treated as cash advances are not possible on Plastiq.

Update 4/18/21: Reposting this since it recently went into effect. I haven’t heard any practical ramifications yet, seems it was more of a warning shot. We’ll see.

Original Post:

Chase sent out an email blast today on both consumer and business credit cards indicating that beginning in April they’ll broaden the cash advance category to include many ‘cash-like transactions’. These transactions would incur a cash advance fee, and won’t earn credit card rewards.

The new rule could make things funding bank accounts, buying crypto, lotto/gambling, P2P payments on Venmo or Paypal, PayPal Key, and even using bill payment services to be considered cash advances. (Plastiq is pretty good at figuring out when their transactions will be cash advance, and I expect they’ll let us know if there are any changes.)

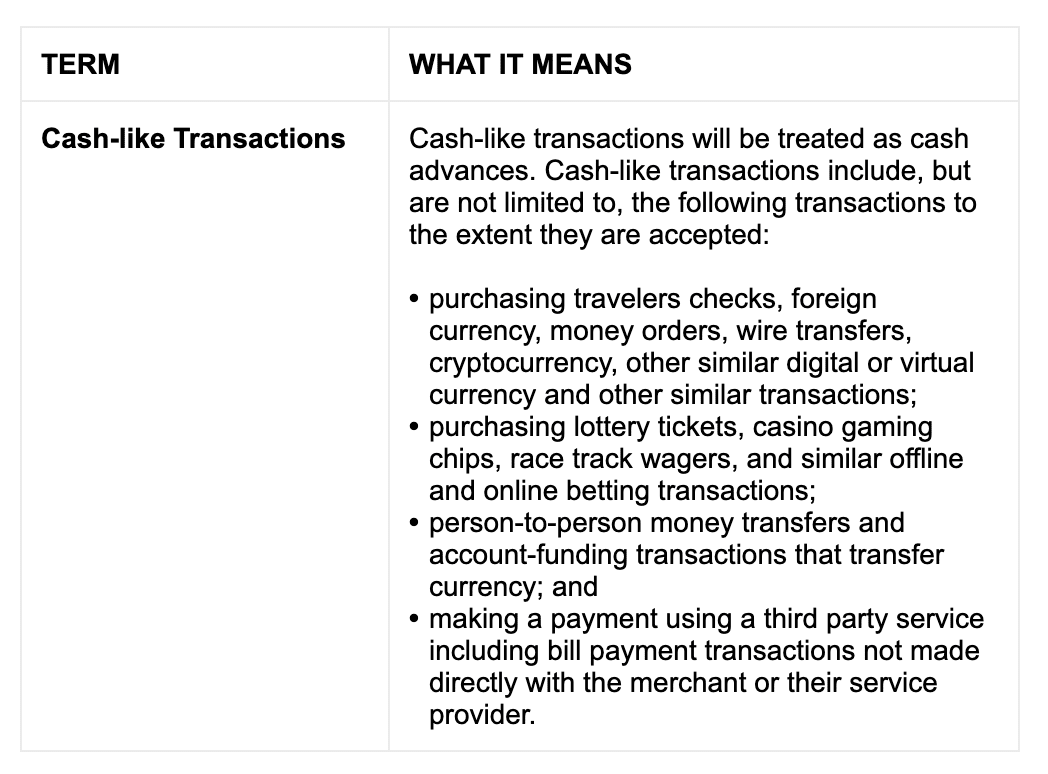

Cash-like transactions will be treated as cash advances. Cash-like transactions include, but are not limited to, the following transactions to the extent they are accepted:

• purchasing travelers checks, foreign currency, money orders, wire transfers, cryptocurrency, other similar digital or virtual currency and other similar transactions;

• purchasing lottery tickets, casino gaming chips, race track wagers, and similar offline and online betting transactions;

• person-to-person money transfers and account-funding transactions that transfer currency; and

• making a payment using a third party service including bill payment transactions not made directly with the merchant or their service provider.

The effective date for this change is either April 10th or 16th with some people seeing one date and some seeing the other. We won’t know for certain how all this will all play out until we get there and see what happens on the ground. Most people got this on Chase business cards, but some are getting this on personal cards too, so it seems it’ll be true across all cards.