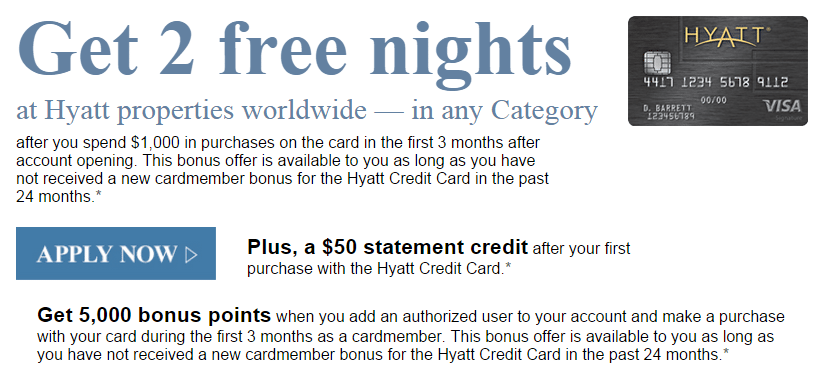

The Offer

- Receive a $50 statement credit after your first purchase, receive two free nights at any Hyatt property worldwide when you spend $1,000 or more within three months of account opening.

- You’ll also receive 5,000 Hyatt points for adding an authorized user and making your first purchase within three months of account opening

Card Benefits

- Annual fee of $75 is waived for the first year

- Card earns at the following rates:

- 3 points per $1 spent at all Hyatt properties

- 2 points per $1 spent at restaurants, on airline tickets purchased directly from the airline, and at car rental agencies

- 1 points per $1 spent on all other purchases

- No foreign transaction fees

- Platinum status as long as you’re a card member

- 1 free night at a category 1-4 property on your card anniversary every year

Our Verdict

It’s been possible to get this offer without the 5,000 bonus points for adding an authorized user for awhile, but it’s good to see those extra points added (and the fact that there is a direct link is also a plus). This is a fantastic bonus, but I’d recommend waiting until you have a plan for your two free night certificates before applying. Obviously in most cases it’ll be better to spend these certificates on rooms that would normally cost more in points/cash and as you only have twelve months to use them by having a game plan it means you’ll get the best value out of this bonus.

Hat tip to Miles to Memories

Chase just matched me to this better offer (+5K points) for adding an authorized user. Thanks for the useful info, again!

Any idea how long this deal will last? Is there a small print with expiration date?

No idea, sorry!

@alan – that’s something I’ve been pondering over as well. it seems like Chase co-branded cards maybe easier as opposed to the UR cards. but it really depends on your recon agent if you end up there, most have had no luck on any Chase card. in any case, the key here (as w/other Chase cards these days) is to get an instant approval.

really wish Chase would just do a soft pull on existing customers if they werent gonna approve you anyways (due to these new internal policy changes.) and ONLY pull if they were otherwise willing to extend you credit, and the hard inquiry would just serve to confirm ones creditworthiness/make sure nothing had radically changed from the customer info they have on you.

I’ve been reading on Flyertalk on how Chase is making it much more difficult to get a card if you have too many new accounts opened in the past year. What’s not clear to me is if this applies to all cards, or only the Ultimate Rewards cards. What do you think?