Update 7/16/20: Chase is now sending out e-mails advertising this feature to some cardholders.

Update 3/28/20: This option is now showing up for some people under ‘things you can do > credit options & tools’

Hat tip to

Last week we shared news that Chase had made a number of changes for current credit cardholders. This included notice that Chase will be launching two new products/features: My Chase Loan & My Chase Plan. We now know that these new products will launch on August 10th, 2019. Let’s take a look at each one in some more detail

My Chase Plan

My Chase Plan gives you the option to pay for eligible charges over a period of time. During this time you’ll pay a rate of 1.72% per month until the full balance is paid off.

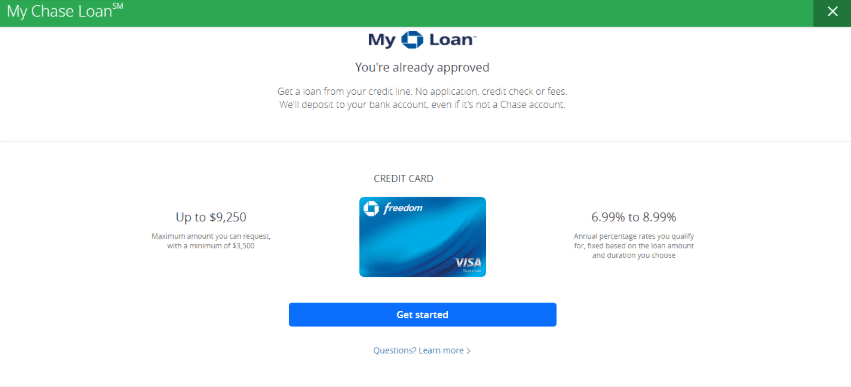

My Chase Loan

My Chase Loan lets you get a loan based on your credit card with Chase, the loan is deposited into your checking account (doesn’t have to be a Chase account). The interest rate you receive will depend on your relationship with Chase but will range from 18-25%.

Our Verdict

Both of these products come with incredibly high interest rates, so I’d be avoiding these as much as possible. My Chase Plan seems to similar to American Express’ Plan it feature and Chase offered something similar called Blueprint in the past as well.