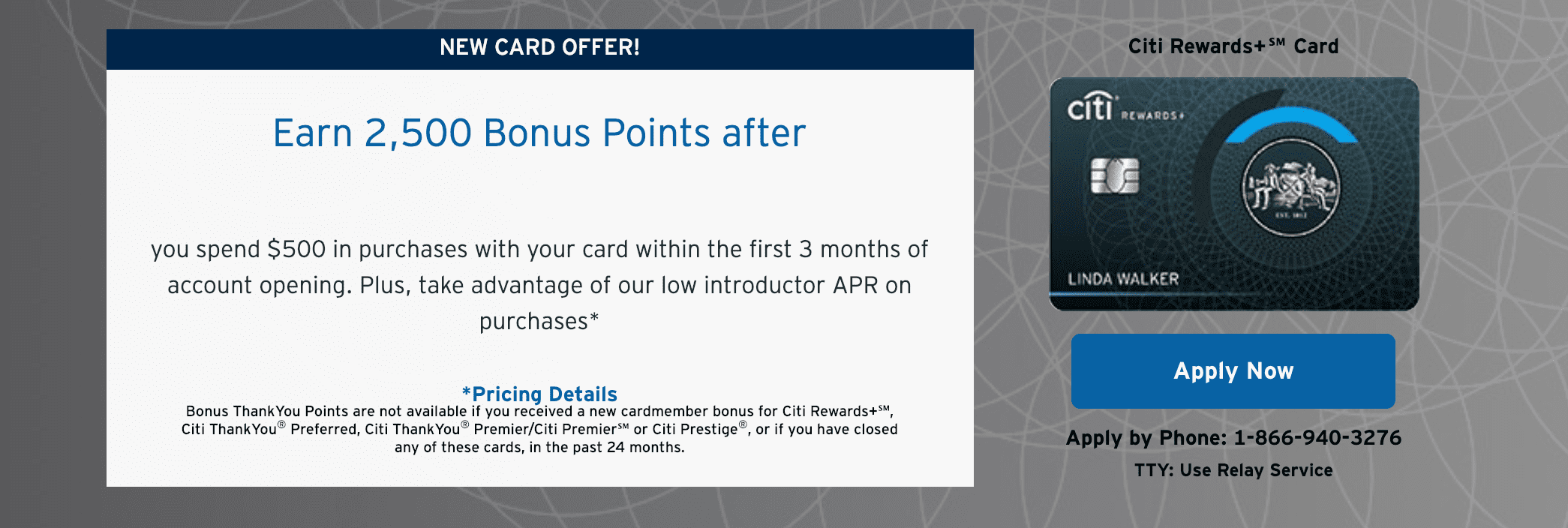

Last week, Citi launched a new no-fee credit card called the Rewards+. Alongside that card, they have a student version as well. Everything about the student card is the same as the regular card except for the lower signup bonus and higher balance transfer fees and rates. You must be a college or graduate student to apply for this card.

Contents

Card Details

To recap again in brief, below are the key details. Check out our post on the standard non-student version of the card for a lengthier discussion.

- Points are rounded up to the nearest 10. For example, a $1 charge will earn 10 points, and a $51 charge will earn 60 points.

- No annual fee

- Card earns ThankYou points

- Earn 2x points on grocery and gas, up to $6,000 per year, then 1x

- Earn 1x points on everything else

- 2,500 points signup bonus for spending $500 within 3 months

- Standard Citi protections

- Bonus ThankYou Points are not available if you received a new cardmember bonus for Citi Rewards+℠, Citi ThankYou®Preferred, Citi ThankYou® Premier/Citi Premier℠ or Citi Prestige®, or if you have closed any of these cards, in the past 24 months

- 3% foreign transaction fee

- 10% rebate on all redeemed points each year, on up to the first 100,000 redeemed points

Our Verdict

No reason to apply for this if you are eligible for the regular card, but this could be a good option for students who have not built up their credit. Not sure how strict Citi is with approvals, but presumably they are much easier with this card than with their others cards (probably with low credit limits).

Other good starter card are the Discover IT and the Chase Freedom. Amex is pretty easy with approvals, especially with charge card, so that’s another option to try.

Hat tip to uscreditcardguide

Related:

- Starter Credit Cards – Best Cards For People With No Credit History

- What Are The Easiest Credit Cards To Get?

- Best Secured Credit Cards

- Shopping Cart Trick 2019 – Get Credit Cards Without The Hard Pull

is this downgradeable from the citi premier would do it to avoid the annual fee and closing the card? also , does downgrading go into the rule that you have spoken about many times in your articles about not being eligible if you open or close the card, does downgradign restart the 24 month clock? thanks

I am sorry but this card is garbage and so was the old ThankYou for college students. I would rather get the ATT card and product change so that it doesn’t affect my ability to get a bonus.

Can you apply for this card if you are 17.5 years old and have a college admission letter for Fall 2019 or do you have to wait till 18?

You have to wait until you are actually 18.

Not sure how to contact you but totally unrelated s just got an email from Ubereats for free delivery on next order using code NEWEATS2019

Subject is:

Hit your 2019 goals with free delivery,

“Your name”

Thanks, Dave! For future my e-mail is [email protected]

This seems like a smart move on Citi’s part. College students would be attracted to the minimum of 10 points per transaction b/c even more than the general population they make lots of small transactions. Plus many will keep the card or product change to another ThankYou point card after graduation through inertia which should gain Citi long term profitable customers.

I guess I feel differently since I am “churner” but as a college student, this card is not attractive at all.

I agree. Definitely not a card for a churner. Not aimed at churners. But maybe attractive to a non-churner who thinks points=good.

I have a debit card that gives 25 cents a transaction so for small transactions, it is a better deal then this.

Which debit card is this?

Foreign transaction fee on website says 3%. If it was actually 4% it would be excessive. But in my opinion all banks should waive the foreign transaction fee.

Fixed, thanks

Trash, DiscoverIt>

I have a discover IT card for MSing the quarterly categories, then I sock drawer the card until the next quarter rolls around.

I still recommend discover cards to people as their first credit card because as far as I know, their secured card is the only one widely available in existence that offers some form of rewards.

Why sock drawer, its 2% for the first year? In my experiences with myself and helping others. They can get approved for an unsecured Discover Card w/ little or no credit history. Agree for MSing quarterly categories as well.

It’s not really 2% though because them holding the money chips away at the value a small bit due to opportunity cost.

Discover It was a great card but due to the heavy devaluations it has faced in the past year or two it’s worthy of being sockdrawered. Sad that it’s lost so many great features like discover deals, price protection, return extension and extended warranty

I miss my 10% back at walmart dearly.

Definitely still a good starter card but beyond that first year, the value dwindles.

That is true and very unfortunate that they did those things. As a first year it is worth it.

I consider 2% unremarkable in the current game. So sure, if you’re new and don’t have a Fidelity Visa, haven’t PCed a Citi card to Double Cash, don’t have a CFU you pair with a CSR for 2.25% on travel minimum, don’t have a BOA travel rewards/premium rewards card and assets with BOA, don’t have another card at 2%+, and don’t have any other cards you need minimum spend to hit, sure, you could use the discover it.

My comments were in regards to a first card. All those cards are not feasible or attainable for someone with limited credit history. Chucks

Chucks