Offer at a glance

- Maximum bonus amount: $1,000

- Availability: Charter One: MI & OH, Citizens Bank: CT, DE, MA, NH, NJ, NY, PA, RI, and VT

- Direct deposit required: No

- Additional requirements: Monthly addition of $25 or $50 in funds

- Hard/soft pull: Soft in branch, hard online

- Credit card funding: Up to $1,000

- Interest Rate: 0.1% APY

- Monthly fees: None

- Early account termination fee: Unknown

- Expiration date: None listed

Contents

The Offer

Direct link to offer (Charter One: MI & OH, Citizens Bank: CT, DE, MA, NH, NJ, NY, PA, RI, and VT)

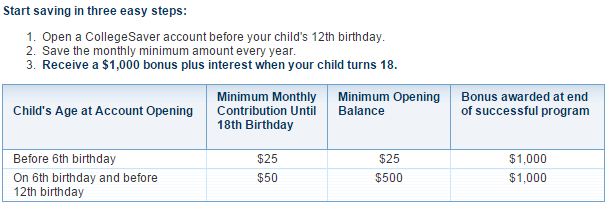

- Receive a $1,000 bonus when your child turns 18 when you complete the following requirements:

- If your child is under 6: Add $25 per month to their CollegeSaver account ($25 opening deposit)

- If your is between 6 and before they turn 12: Add $50 per month to their CollegeSaver account ($1,000 opening deposit)

The Fine Print

- All bank account bonuses are treated as income/interest and as such you have to pay taxes on them

Avoiding Fees

This account has no monthly fees and you’ll need to keep it open for 6-12 years so any early account termination fees should not be an issue.

Analyzing The Deal

Let’s see if this account makes sense, the interest rate is only 0.1%. It’s easy to find deposit accounts that earn at least 1%, you can also get 5% if you put the money in a rewards checking account although this would require a lot more management.

Before 6th Birthday

This assumes you set up the account just before their 6th Birthday

- Charter One / Citizens Bank: $3,647 + $1,000 bonus

- 1% account: $3,853

- 5% account: $4,948

The 5% account is the better performer by far, but this would require a lot more management. It’s also not that big of a difference ($308). The 1% account was the worst performer out of the three.

Before 12th Birthday

This assumes you set up the account just before their 12th Birthday.

- Charter One / Citizens Bank: $4,617 + $1,000 bonus

- 1% account: $4,773

- 5% account: $5,531

This time the $1,000 beats out all challengers and is the best option, although the 5% account is not far off.

Our Verdict

Your best bet would be to wait until just before your Child is 12 and then set up this account for them. Obviously in the real world this isn’t feasible because the deal might not be around when they are 12. I don’t have any kids so I won’t be participating in this deal, if I did have kids then I’d probably set up an account for them. It’s not required to spend the funds on education, so the money and bonus is actually pretty flexible.

The only concern is that interest rates go up dramatically and this account does not up their rates as well. I think the chances of this happening are relatively low, but it’s difficult to predict that with any level of certainty when you’re looking 6 or 12 years into the future.

Our bank account bonus page will now start to include savings accounts, as well as the usual checking accounts and business accounts.

Direct link to offer | Screenshot of offer

Thanks to EIG for letting us know about this bonus, she could win up to $225 for letting us known.

{kind=link}

Hello, I was able to fund 2 savings accounts I opened online with Chase Southwest Cards. Personal Priority and business preferred. (I had previously opened a checking account online a few months ago). The reason i opened 2 was actually by accident. The first one I opened I did not see a pending charge on my card (probably because it was a holiday Jan 1st) so I tried the other card and same thing happened so I just waited it out a day or 2. Online it sowed the accounts but no money then a day or 2 later i saw the charges pending and deposit pending. Everything posted by day 3 or 4. This was done on Southwest Priority and the Southwest Business preferred.

Oh and its $1,000 each savings account for a total of $2,000. Cheers!

Not a DP but just two cents: Great deal if you are ineligible for financial aid already. If you are eligible or on the borderline, this can be a risky move. Colleges look at all assets, funds, retirement savings, etc owned by the parents when determining the aid– but obviously its not 1:1 ratio (ie if you have 10k more in savings, they wont decrease the grant by 10k.) but college savings are taken as 1:1 ratio, because its usage is exclusively for college.

You are better off putting it in another savings account if you are aiming for a decent financial aid package. If your net worth makes you ineligible for aid anyway (and I assume most readers here are, being financially smart), this is great.

This account is converted to a regular savings account shortly after the child’s 18th birthday. For financial aid purposes, there would be no difference between this account and any other savings account in your child’s name. Funds do not have to be used for college expenses.

I know there haven’t been any comments here so maybe no interest but just a DP (and it is still alive BTW with $1,000 CC Funding).

I wanted to open one of these with Citizens – was hoping to use a Marriott CC that was approved over a week ago. Kept waiting hoping it would show up. Daughter turns 6 on Saturday…

So the Marriott card hadn’t showed by yesterday so I went to open it up with a SW card and I cut it too close. You need to open the account at least 2 days prior to the 6th (or 12th) birthday to do it online. I was trying to do it last night around 11:45pm and it all was working and then I went back to make sure something was right on the application and midnight passed and it wouldn’t work anymore – it kept saying she was already 6!! If I changed her birthday to Sunday it worked though…crazy that midnight passing screwed it up! Tried again this morning, still no luck.

I went to the branch (as instructed to do over the phone) and they couldn’t do CC funding in branch (even though the phone CSR said they could). I then called again this afternoon and was able to open the account over the phone and credit card fund.

Will post back if any issues but at this point looks like I was able to open the account with $1,000 on a SW Chase Card.

Southwest Visa posted $1,000 as PURCHASE

Thanks, added