This is the first post in our series that compares different credit scores. In today’s issue we are going to compare FICO scores & PLUS scores. We’re going to look at the scoring factors that causes them to be different, their ranges, who uses the score and where to get the scores from.

Comparison Table

| FICO Score | PLUS Score | |

|---|---|---|

| Minimum Score | 300 | 330 |

| Maximum Score | 850 | 830 |

| Median Score | 723 | 724 |

| Available to Individuals | Yes | Yes |

| Acessible for Free | Yes | Yes |

| Used by Lenders | Yes | No |

| Scoring Criteria | ||

| Payment History | 35.00% | Not public |

| Credit Utilization | 30.00% | Not public |

| Length of Credit History | 15.00% | Not public |

| Types of Credit used | 10.00% | Not public |

| Recent Searches for New Credit | 10.00% | Not public |

Unfortunately the PLUS scoring team doesn’t make their scoring criteria public, but have stated numerous times that it’s “remarkably similar to the FICO score” so we can only assume they use similar scoring metrics.

Both scores are available for free, when you sign up for a credit monitoring program and cancel before the trial period ends. We suggest using myFICO’s “Score Watch” for your free FICO score and freecreditscore.com if you want a PLUS score.

The biggest difference between the two is that the FICO score is used by lenders and the PLUS score isn’t. We’ve said this numerous times but it’s worth repeating, FICO is used in 90% of lending decisions.

If you just want a broad idea of how your credit is (e.g poor, good, excellent etc) then the PLUS score should be able to do the job. If you’re applying for credit and want to see a score similar to that of what a lender will see (there are 49 different FICO scores after all) then we suggest looking at your FICO.

How Do The Scores Compare?

I decided to compare my scores between the companies so you’d have a real example of how they differ. Because the PLUS score is based on Experian data, I decided to find out what my Experian FICO score was. The only Experian FICO score currently available to consumers is the 2004 classic score, also called EX-04 FICO or Experian, FICO Risk Model V3. This is available from myFICO.com and I picked up my copy for $15.95 by using a promo code “E1311BDY20FST” (click here for up to date promo codes). If I didn’t care about the credit bureau then I could’ve used the Score Watch product and got it for free.

I then headed over to http://www.freecreditscore.com to get my PLUS score. Below are the results:

| FICO | PLUS | |

|---|---|---|

| My Score | 821 | 799 |

As you can see, there is a score difference of 22 points. A lot of forum posters have higher PLUS scores than FICO, one of the reasons mine might be the inverse is because of how high my score is and that the PLUS’ top score is 830 whilst FICO is 850.

If you know both your PLUS score & your FICO, let us know what they are in the comments.

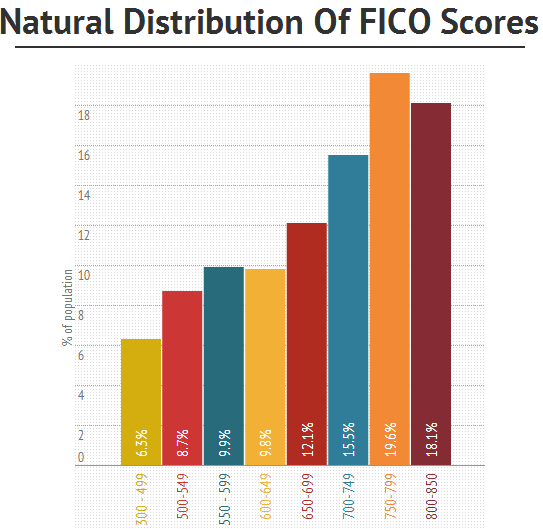

Graphs of natural distributions of both of the scores below for the graph lovers out there.

I just learned that my credit score according to Plus is 654, and that Fico is 776. Hmmmmm. Huge difference. Experian told me that lenders do not use Plus scores, but that is exactly the score that they gave my lender. Experian also told me that they have not used Plus since March 2017, and that it was used for educational purposes.

On the community forums of USAA a “community manager posted this:

Briana Hartzell USAA

Community Manager

dustinator,

Here are some facts about the credit monitoring program I got from an expert here at USAA. I hope they help answer any concerns you have.

The Credit Check Monitoring Service utilizes a PLUS Score model, with scores ranging from 330 to 830, it is a user friendly credit score model developed by Experian to help you see and understand how lenders view your credit worthiness. It is not used by lenders, but it is indicative of your overall credit risk. As you are aware, there are three different major credit reporting agencies, Experian, TransUnion, and Equifax that maintain a record of your credit history known as your credit file. Your Credit Score is based on the information in your credit file at the time it is requested. Your credit file information can vary from agency to agency because some lenders report your credit history to only one or two of the agencies. So your credit score can vary if the information they have on file for you is different. And since the information in your file can change over time, your Credit Score may be different from day-to-day.

Lenders and insurers use several different credit scoring models which could explain why your lender gives you a score that is different from the PLUS Score you receive online. Just remember that your associated risk level is generally the same even if the number is not. The importance of the Credit Check Monitoring service is to help members ensure the information reported on their credit file is accurate; even though the provided credit score was different the information on the report is the same.

The Plus Score is calculated using the following factors:

31% Payment History and Bankruptcy

30% Credit Card Debt

15% Length of Credit History

14% Type and Number of Credit Cards

10% Credit Applications/ Inquiries

The point range of the scoring models may be different as well which can account for the number not being the same:

Experian’s PLUS Score range is 330 to 830

Transunion’s Empirica score range is 150-934

Equifax’s Beacon Score range is 300-850

FICO score is between 300 – 850

The Vantage Score range is 300 – 850

This would provide the numbers you are missing from your article.

My FICO is 826, PLUS is 728. That’s a huge disparity. I’m just glad the lenders don’t look at PLUS scores.