This is the second post in our series that compares different credit scores (first post we looked at FICO Score Vs PLUS Score). In today’s issue we are going to compare FICO scores & VantageScores. There are actually three versions of the VantageScore (1, 2 and 3), because version 3 changed the range of scores we’ve separated it and we will actually be comparing three different scores today: the traditional FICO score, VantageScore (Versions 1 & 2) and VantageScore (Version 3).

This is the second post in our series that compares different credit scores (first post we looked at FICO Score Vs PLUS Score). In today’s issue we are going to compare FICO scores & VantageScores. There are actually three versions of the VantageScore (1, 2 and 3), because version 3 changed the range of scores we’ve separated it and we will actually be comparing three different scores today: the traditional FICO score, VantageScore (Versions 1 & 2) and VantageScore (Version 3).

Comparison Table

| FICO Score | VantageScore (V1&2) | VantageScore (V3) | |

|---|---|---|---|

| Minimum Score | 300 | 501 | 300 |

| Maximum Score | 850 | 990 | 850 |

| Median Score | 723 | N/A | N/A |

| CRAs the score is based on | EX, EQ & TU | EX, EQ, TU | EX, EQ, TU |

| Available to Individuals | Yes | Yes | Yes |

| Acessible for Free | Yes | Yes | Yes |

| Used by Lenders | Yes | Yes | Yes |

| Scoring Criteria | |||

| Payment History | 35.00% | 28.00% | 28.00% |

| Credit Utilization | 30.00% | 23.00% | 23.00% |

| Length of Credit History | 15.00% | 9% (called depth of credit) | 9% (called depth of credit) |

| Types of Credit used | 10.00% | 0.00% | 0.00% |

| Recent Searches for New Credit | 10.00% | 30.00% | 30.00% |

| Credit Balances | 0.00% | 9.00% | 9.00% |

| Available credit | 0.00% | 1.00% | 1.00% |

FICO & VantageScore have a lot of similarities especially with Vantage moving to a more traditional range of 300-850 in version 3 of their product. Both scores are used by lenders (Vantage is thought to be used in around 5-10% [5.7% according to court documents filed in 2006] of lending decisions with FICO being used in 90%) and both are available for free to consumers.

The easiest way for a consumer to get a free vantage score is through Credit Karma or Quizzle, whilst they can get a free FICO in a number of different ways.

Looking at a VantageScore is a great way to understand the over all health of your credit, whilst looking at a FICO score is a great way to see if you’ll be approved or denied for a loan before applying (obviously they look at other factors such as employment history & income, and will most likely look at an industry specific FICO score which isn’t the same score as you see).

How Do The Scores Compare?

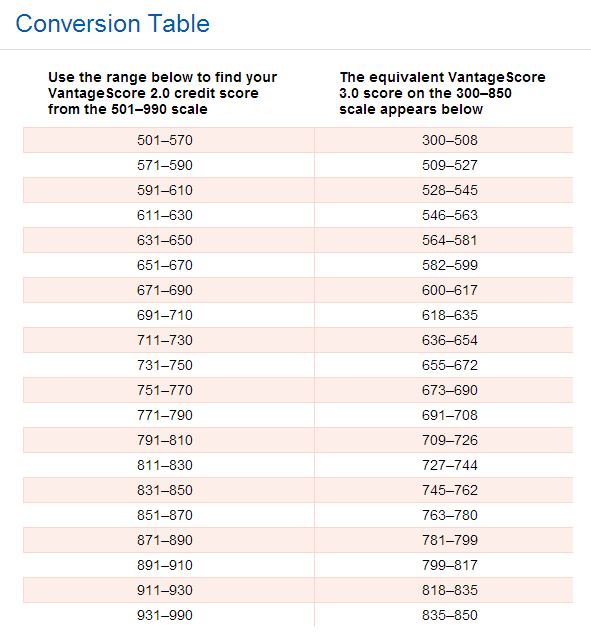

Because I’d already purchased my Experian FICO score from myFICO, I decided to purchase my VantageScore through Experian ($7.95) so we’d be comparing apples to apples. It also meant I was able to get version three of my score, which can be roughly converted using this conversion table.

| FICO | VantageScore (V1 &2) | VantageScore (V3) | |

|---|---|---|---|

| My Score | 821 | 831-850 | 746 |

As you can see my VantageScore is significantly lower than my FICO score when converted to the same range (300-850 instead of 501-990). There are a couple of likely reasons for this, VantageScore puts more weight on recent searches for new credit (30% instead of 10%) and less weight on payment history (28% vs 35%).

I have a flawless payment history, with no late or overdue items. I’ve also made a number of credit card applications to make the most of sign up bonuses (read our introduction to churning if this interests you).

As both of these scores are used be creditors, it’s a good idea to keep track of them. Credit Karma offering the VantageScore for free means there is no reason you shouldn’t know yours before applying for new credit. There are also a whole heap of ways to access your FICO score for free.

Editors note: All credit scores were purchased on the same day within an hr of each other and nothing that affects credit scores was changed within this time period (including the PLUS score which was seen in last weeks article – as the articles are written at the same time and then released weekly as part of the series).

If you know both your scores, let us know what they are in the comments.

{kind=link}

Apparently there is now VantageScore 4.0

https://www.creditkarma.com/advice/i/new-vantagescore-4-0-explained/

and according to an MF forum thread

https://ficoforums.myfico.com/t5/Credit-Cards/Sync-PPMC-to-use-Vantage-4-0-for-CLI-s/td-p/5750564

it is being used by Synchrony Bank, at least for CLIs.

On reading that MF forum thread, some are questioning whether VantageScore 4.0 was actually used for a credit decision (as was reportedly claimed by some random CSR who may not know what they’re talking about.)

Just to chime in with my experience, my student loan company (a Texas-backed loan company) uses Vantagescore to approve new borrowers. I was in a bit of a panic because I had several new accounts with high balances (paid my tuition to get sign up bonuses) which destroyed my VantageScore. Luckily, you need a 650 Vantage to be approved, and I had a 655!

No creditor I know of uses VantageScore, although DoC article says 5-10% do. All the big banks I know of use FICO. Consider VantageScore like a rough estimate. I assume the credit help websites use VantageScore because it’s cheaper… FICO probably charges more? So, I’d be willing to bet that 5-10% of lenders are shady pay-day lenders and 2nd chance CC’s that are too cheap to pay more.

As I recall, you closed out of a lot of accounts. That is going to sting. But continue to look at banks that give FICO scores for a better gauge of where you are at. See:

https://www.doctorofcredit.com/free-fico-scores/

Also, the rule of thumb it takes about 3 months to mostly recover from an app-a-palooza. So, keep that in mind that time does heal (most) all wounds.

Vantage3 is much more persnicketty than FICOs about some things, which causes much bigger swings, e.g. high util one one card, even if low util overall – but there are also a few other things that seem to make V3 cry wolf.

P.S. Wow this is an early DoC thread.

There is frequent comment about the variance in individual’s FICO and VantageScores but for what it’s worth I can state that in my case the scores are almost exactly the same across all three CRAs as of this posting in January of 2018.

If both Credit Karma and Quizzle use the same V3 scoring, any ideas why is there such a large difference in my indicated scores? (Credit Karma 693, Quizzle 746). Thanks for any feedback.

Are you comparing your TransUnion CK score or your Equifax? Quizzle just uses Equifax, so if you’re comparing your TransUnion score on CK then it’s because they contain different data.

I’m confuse with my credit score cause on credit Karma my score is 617. So we’re deciding to buy a house but I went to see lender they check credit score was only 530.i don’t understand

The score Credit Karma gives you is different to the scores most lenders use.