Fidelity introduced today a new benefits program for actively managed wealth management clients. It’s called Fidelity Rewards+.

Direct Link to Fidelity Rewards+

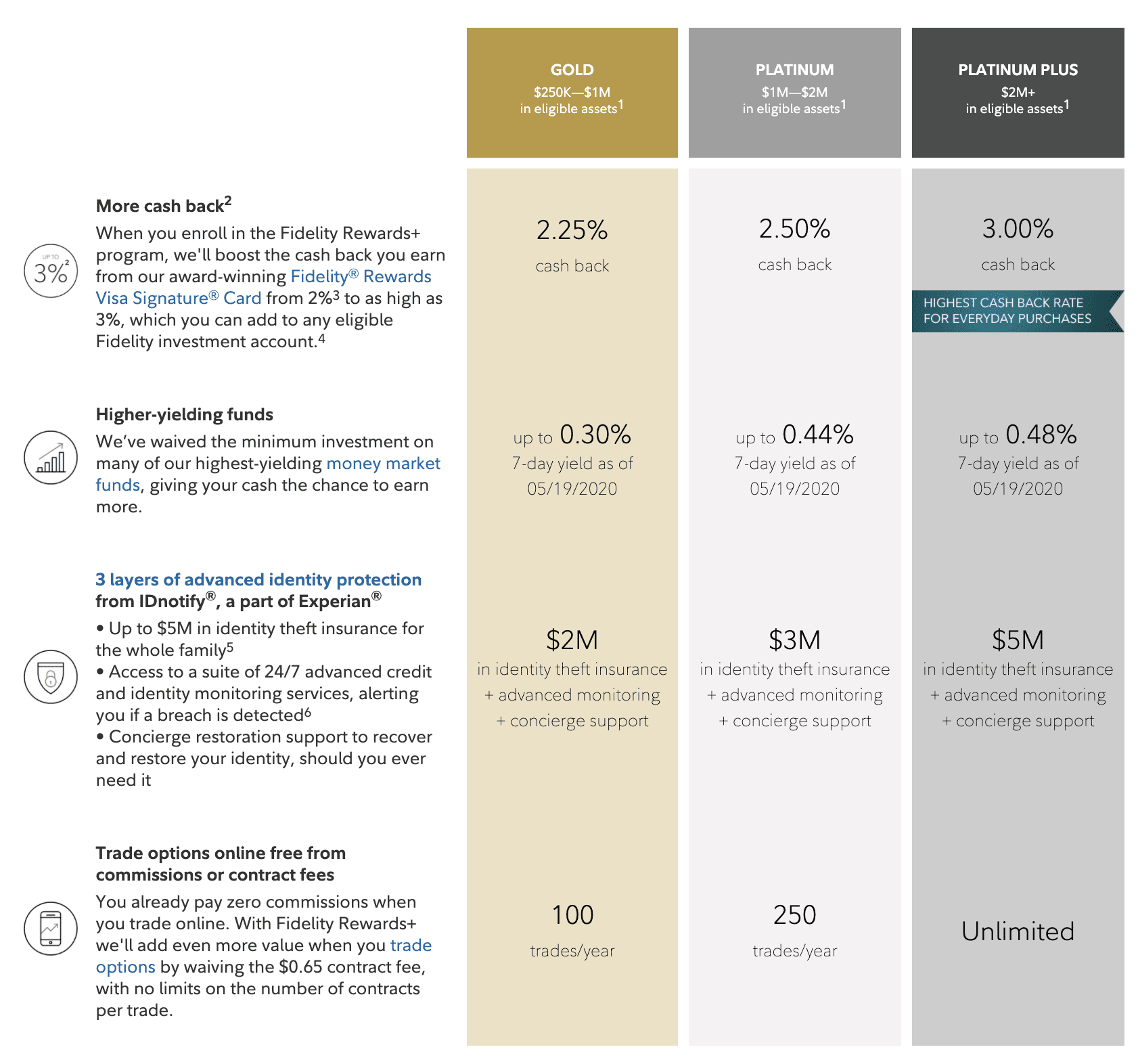

Overview

Fidelity launched today the Fidelity Rewards+ program for wealth management customers which offers up to 3% cashback on the Fidelity credit card (instead of 2%), free options trading, higher-yield funds, and identity protection. There’s also a time-limited $75 signup bonus.

There are three tiers of benefits:

- Gold for those with between $250,000 and $1M in assets

- Platinum for those with between $1M-$2M in assets

- Platinum Plus for those with $2M+ in assets

It’s free to join Fidelity Rewards+, and benefits are kept for 1 full year and renew automatically.

Benefits

- Fidelity offers the 2% Fidelity Rewards Visa Signature card which has no annual fee. Fidelity Rewards+ members can earn up to an additional 1% for a total of 3% cash back on everyday purchases that can be added to any eligible Fidelity investment account.

- Gold members get 2.25%

- Platinum members get 2.50%

- Platinum Plus members get 3%

- Fidelity Rewards+ members can invest in many of their highest yielding money market funds without the typical investment minimums, providing the potential to earn more.

- Fidelity Rewards+ members get access to three layers of ID protection: up to $5M in identity theft insurance for the whole family, access to a suite of 24/7 advanced credit and identity monitoring services that alerts the customer if a breach is detected, and concierge restoration service to recover and restore a customer’s identity, should they ever need it.

- Fidelity Rewards+ members can trade options online free from contract fees for up to an unlimited amount of trades.

- Gold members get 100 free trades per year ($65 value)

- Platinum members get 250 free trades per year ($162.50 value)

- Platinum Plus members get unlimited free trade per year (variable value)

$75 Signup Bonus

Be one of the first 10,000 to enroll in Fidelity Rewards+ and you’ll get a $75 credit when you make any Amazon purchase (no minimum) using the Fidelity Rewards Visa Signature Card by 9/30/20.

Our Verdict

The 3% is a nice benefit, and the free options can be a real money-saver to those who trade options. The big catch here – aside from the actual money requirement – is that there is an annual advisory fee of .5%-1.25%; on $2M it would amount to around $20,000 per year. It’s highly unlikely to be worth a $20,000 annual fee in order to get the extra 1% cashback on the credit card and some free options trading.

This new program rivals others like the Bank of America Preferred Rewards program which offers up to 2.62% cashback on all purchases for relationship customers. There aren’t any other credit cards that earn 3% across the board. On the other hand, Bank of America counts passively invested funds and retirement funds in their balance tier requirements, so there’s no cost to get the benefits, making much more useful to a lot of people.

Some people might want an active investing manager (not something I’d typically recommend, but there are probably scenarios where it could make sense), and then the 3% credit card cashback rate would be an added little bonus. Overall, I don’t see this program as being useful to many people.

Hat tip to my friend Jon

Note that before the last round of tax reform, these “advisory fees”were tax deductible which made them slightly more tolerable.

Also note it’s not uncommon for senior management in publicly traded organizations, to receive reimbursement for “advisory fees” as an employee benefit, for themselves and potentially “extended” family. I suspect this is because it’s better for corporate officers to completely avoid trading in the markets with personal or family money.

This doesn’t seem to rival Bank of America’s program in the least.

Just $100K parked in cheap index funds at Merrill can get you 2.625% back on every day spend with Preferred Rewards.

Compare that to $2MM at Fidelity with a management fee, just to get back 3% on a card?

BofA/Merrill for the win. Not even close.

but you don’t get unlimited option trading for free at BOA /s

Lol

People who care about trading options aren’t going to use Fidelity regardless.

Honestly, a $6,600 annual fee to play with unlimited options in a “beer money” account, while also paying for professionals to maximize fake losses to offset gains elsewhere sounds intriguing. But I don’t have $2 million taxable to invest, and for that level of speculation why wouldn’t you go to IB with its sub-1% margin interest rate?

You could participate in the Separately Managed Accounts and qualify. It’s basically rolling your own actively managed mutual fund, and the expense ratios are lower than the comparable actively managed Fidelity funds.

https://www.fidelity.com/managed-accounts/separately-managed-accounts/overview

https://www.fidelity.com/bin-public/060_www_fidelity_com/documents/SD-program-fundamentals.pdf

For example, the Separately Managed bond strategy has an expense ratio of 0.40% (up to $3 million). The Fidelity bond ETF (FBND), which is actively managed, has an ER of 0.36%. https://screener.fidelity.com/ftgw/etf/goto/snapshot/snapshot.jhtml?symbols=FBND

For $2 million in the Separately Managed Tax Managed Equity strategy, the net fee after tiers is $6,600 (0.33%). While FNILX (the Fidelity large cap index zero fund) is obviously 0% fee maybe the ability to generate phantom losses through tax management is worth $6,600 to someone with $2 million in assets. I don’t know. https://www.cnbc.com/2017/09/26/tax-efficient-customizable-investments-try-a-private-portfolio.html

“ The big catch here – aside from the actual money requirement – is that there is an annual advisory fee of .5%-1.25%; on $2M it would amount to around $20,000 per year. It’s highly unlikely to be worth a $20,000 annual fee in order to get the extra 1% cashback on the credit card and some free options trading.”

Fidelity can’t be stupid. They must expect rich people to pay this amount right?

I wonder who in the marketing team decided the 75$ bonus would do the trick for someone willing to let go of 250k to their hands, just to then add an amazon purchase requirement to it

maybe it is (partially) paid by amazon

I’m not sure I understand why they’d even bother with this. Do people with 250k-2m+ of *actively managed* assets really care about 1% extra on the fidelity credit card? The higher yield is worthless and at 2m of assets, my option trades better be free. I’m not even going to bother commenting on the ID protection

This. I mean, I understand someone with that much money is probably a big spender so the extra 1% would be “significant” (sort of) to an average person, but it wouldn’t be significant to them at all.

I’m sure there’s a lot of people with $2m of assets who don’t care about an extra 1%, just as there are people with little to no assets who don’t. But at what point do you think someone who does (i.e., the sort of people who read this) would stop? For better or worse, I doubt I’ll ever get to the point where I say “I have enough money, I don’t care about cash back anymore.”

The people who read this aren’t going to have $2m *in actively managed accounts with fidelity*. It’s not about “enough”, it’s about caring about 1% extra credit card cashback AND paying .5%+ for someone to buy index funds.

> paying .5%+ for someone to buy index funds

If someone is a sucker enough to pay that overhead, I’m sure they’ll be steered to actively managed funds as well.

I don’t not care about cashback anymore, but I am at the point where I’ve stopped caring about putting in tons of effort for marginal gains. I often don’t care about Discover/Chase 5% categories because the effort to put some handful of purchases on it just isn’t worth my time.

With the Priceline rewards visa I’m at basically 3.5%+ back on everything, 3x Citi AT&T access more card on online purchases, 4x Amex Gold for grocery/restaurants, Altitude Reserve for 4.5% on remote pay and gas/hotels… extra gains are kind of minimal.

How do you get 3.5%+ with Priceline VISA card? Even if you redeem them for travels they’re worth around 1.9% ish.

You’re looking at this all wrong; this isn’t being marketed to us.

It is mostly a marketing gimmick… the managed funds fees they charge are competitive with what other brokers are charging, so this helps them stand out from their peers and can serve as the one additional benefit that engages that new customer where they might have otherwise used a competitor.

Also, many wealthy individuals don’t necessarily “penny pinch”, but they’re often still frugal, so when they hear about things that are “best in class” offers, they typically will consider them. Being frugal is often how many become wealthy in the first place.

It also adds to the stickiness of the client. Just another reason for them to stay.

Look at it another way: If you were trusting them to manage $2m, wouldn’t you expect the best cash back rate in the market? If you’re paying $20k a year to have them manage your money so you don’t have to, would you be pleased about needing to shop around for a better card and log in to multiple banks? Would you want to screw with travel rewards points to squeeze out a couple extra percent, or would you just want the best no-hassle cash back?

2mm is a halfway-ish number.

Still far from anything that actually has ‘private’ in the name (minimal is usually 10mm) but quite a bit beyond ‘cheaper’ options like CPC, BOA’s “Preferred Rewards” or Citi gold.

Fido is essentially creating a more granular tier in their product line to cater for those with more than 250k but less than 10mm invest-able assets, I assume other banks/brokers will follow suit soon.

“Do they care about 1%?” One answer maybe as there’s little other options, even when the other options pop up they gonna be quite similar, so why say no to another 1%?

Ooof, yeah the fee is a killer. Thought I could park money in Fidelity’s zero fee FZROX and reap additional rewards…

Yep, I really should just start reading “Our Verdict” first. Love how Chuck and William give it to us straight.

Thanks 🙂

Updated the title to make it even clearer.

Grant that’s exactly what I do, skip straight to the Verdict. It’s the original TLDR, or BLUF for those in the know.

Have the funds with them and the card, but no way with that 0.5% fee (at least $1250 a year), and that’s if their “professionals” don’t lose any of your money…

Same. It’s bad enough they use Elan to manage the credit card.

And the at least .5% fee is only for Funds/Assets after $5 million

Average Daily Assets Annual Gross Advisory Fee

First $500,000 1.25%

Next $500,000 1.10%

Next $1,000,000 0.90%

Next $3,000,000 0.70%

More than $5,000,000 0.50%

Ahha, I see, so it’s actually more than $10k in fees on $2M invested. I’ll update, thanks

Yeah, you pay 1.25% on the first $500,000. Then from $500,001-$1,000,000 you pay 1.10%. So even if you have $10 million you would be paying 1.25% on the first $500,000 of it.