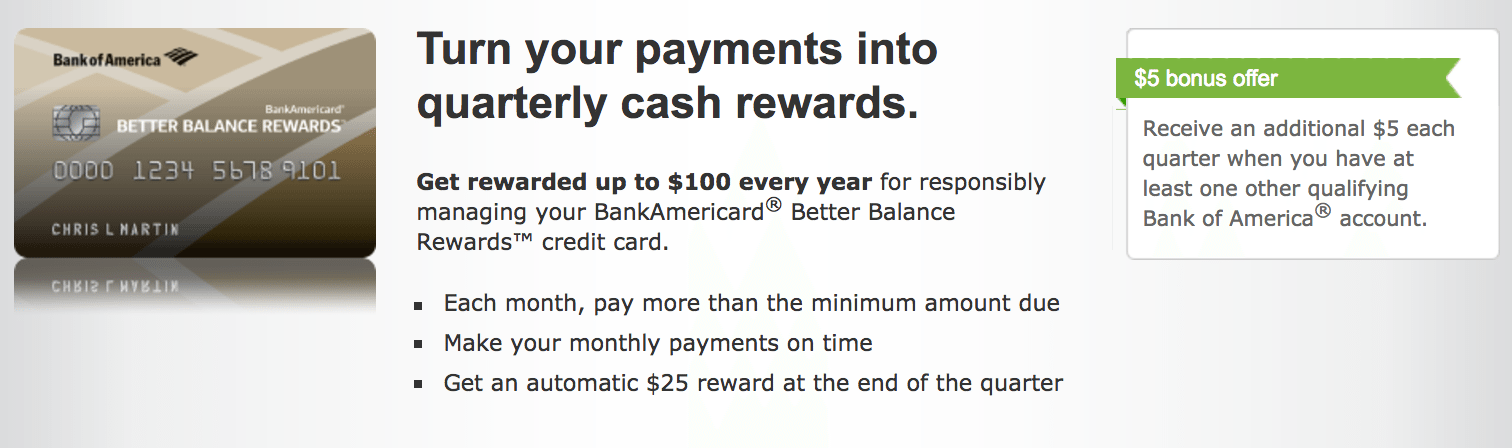

The Better Balance Rewards card from Bank of America offers $25 per quarter when you pay more than the minimum of your balance or pay it down completely each month.

You can apply for the card directly. Many people choose to product change another Bank of America card into a BBR card. It’s not always easy to do since lots of reps will say it’s not an option, but there have been recent success stories.

Read: Product Change Your Useless BofA Cards And Earn Up To $120/yr Per Card

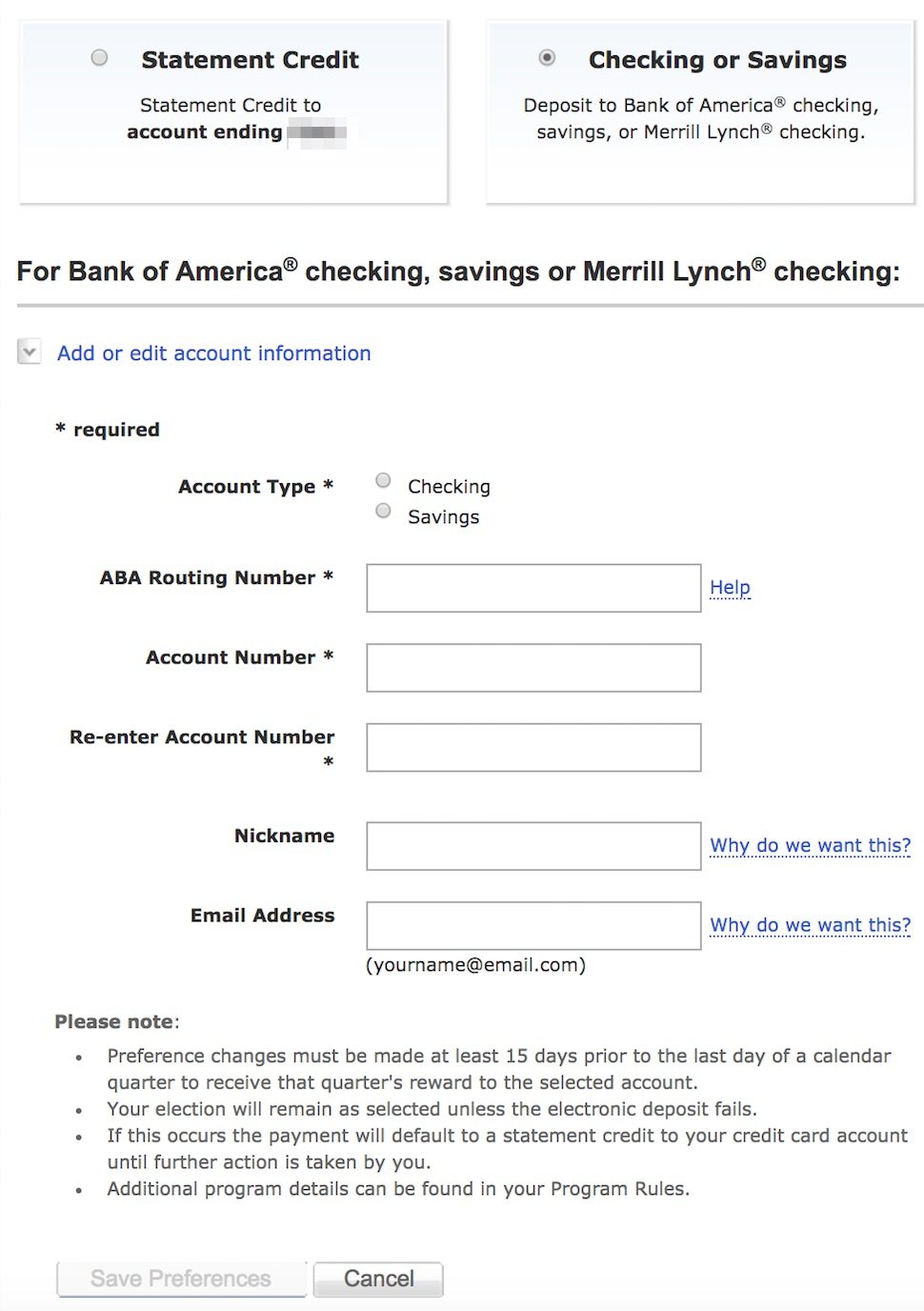

You can get the $25 as a statement credit or as a deposit into your Bank of America or Merrill Edge checking or savings account.

If you have a Bank of America checking or savings account or a Merrill account, you’ll get an extra $5 each quarter. You’ll end up netting $120 each year instead of $100.

I used to think you need to have to choose to have the bonus deposited into your BofA checking/savings account, but I just learned that so long as you have one you’ll get the bonus even if you choose the statement credit option.

In any case, choosing to deposit it into a checking or savings account makes it easier to automate the purchase and payment since if the $25/$30 comes back as a statement credit, you’ll have to then spend that amount on the card. On the other hand, if you choose the bank option, you can charge a steady amount each month, have it auto-paid, and never have to think about the account.

We recommend putting a minimum of $5 per month on the card so as to avoid the possibility that Bank of America will randomly forgive the balance which will disqualify you from the bonus. There have been a number of reports of this happening.

An easy way to do automate this is to put any recurring subscription, such as Netflix, on the card and have it auto-paid. Or automate a $5 Amazon Allowance load to your account each month and have it auto-paid.

How to Change your Selection

So how do you select where the $25/$30 should go – as a statement credit or your bank account?

I was recently struggling with this and couldn’t find anywhere in the login to do so. Luckily, and informed rep was able to direct me to where it’s possible to do this online with no human intervention.

bankofamerica.com/betterbalancerewards

After logging in, you’ll see this:

Choose the Checking or Savings option, add your routing/account info (it won’t pull up automatically), and click Save Preferences.

So, I may be the only doofus that did not realize this, but just as a heads-up: The quarterly calendar for payouts goes by payment DUE DATE and NOT by statement closing date. For example, for Q1, your quarterly reward will be paid out in April if you pay more than the minimum balance (or payment in full) on or before the stated due date on your December, January, and February statements (which will have due dates in January, February, and March, respectively).

I got tripped up on this because, for my BBR statement that closed in April (due date in May), I got a small balance adjustment when my statement posted, bringing my balance due to $0.00. Realizing that my Q2 reward would not be paid out as a result, I wrongly decided to not use my BBR card for the statements that closed in May (due date in June) and June (due date in July), thinking that the quarterly calendar went by statement posting date. I restarted using my card in July, only to learn today, after speaking with a Bank of America rep, that I missed the Q3 bonus as well for not having a balance due on my June statement (due date in July).

Needless to say, I won’t be making that same mistake again, but I just thought I’d alert others to it, as well, if you temporarily stop using your BBR card for whatever reason.

Wow, wish I knew about the option to set the rewards to be deposited to my checking before. I had the bonus post and set my balance below $0 numerous times, which then mess up with my next quarterly rewards. Thank you SO MUCH! Just made my life a lot easiler.

is there a 1099-int for the bonus eared by paying off bbr balance?

No.

FYI, found this: https://www.managerewardsonline.bankofamerica.com/cms/published/root/dcb/PDF/BBREng045644June2016.pdf

It provides all the details of the program. I like that it gives a No Later Than date for the reward payment.

I fully expect NOT to get my bonus from the 1st quarter of this year, because I did not pay more than the minimum due, and I let the balance hit zero during the middle of the month, even though I had at the end statement each month with a balance due. I paid the full balance, which was the minimum due, and then charged something new each month; repeat. I will post if I am incorrect. In the future, I SHOULD find a monthly recurring bill that I can auto pay with this card so there will always be a balance.

You should be good to go — read the language about qualifying payments 🙂

Yeah, I just caught that. But everywhere else it says a qualifying payment is one that is more than the minimum due. I guess I will find out NLT April 30th. I got the card in December, and it seems like forever to get this money train rolling.

Yesterday I received my 1st $30 rebate into my BOA savings from the BBR.

Listed as: 04/05/2017 FIA CARD SVCS DES:CASHREWARD ID:MYLASTNAME INDN:longnumber CO ID:shortnumber PPD

So, paying the monthly bill anytime AFTER the bill has been generated doesn’t matter, as long as it is not late. Just have to have spend each month, and let the bill get generated before paying it off. Reward payout occurs in Apr, Aug, Oct, and Jan, after each calendar quarter.

Some commenters in the BBR Doc blogs said:

A: you cannot ever let the DAILY balance touch zero – This is FALSE. I paid my balance in full, then charged something else during the same statement cycle. As long as you owe something at the END of all the monthly statements, you are good to go.

B: you must pay more than the minimum payment – This is FALSE. Only true if the minimum payment is LESS than your balance. If you minimum payment IS the balance, you can pay it off exactly and still get the bonus.

Someone also suggested in one of the BBR comments that maybe BOA had came out with new terms, and some others were grandfathered to be able to get the reward with a small balance paid off each month. Well, I opened my account in December 2016, so it is about as new as can be to get the reward.

Grrr. Correction – payout in Jan, Apr, Jul, Oct. Not AUG.

DP: I was able to call Bank of America, and PC 2 credit cards I don’t use anymore (a Travel Rewards and a Preferred Rewards) into Better Balance Rewards cards. It was easy and painless.

I realized how little I knew about credit cards, rewards, and overall better managing my finances. But in the last 2 months, I have learned so much, and I cannot stop anymore 🙂

The BOA card services called me today and said that they denied my request to do a PC on those two cards. Bummer.

I have an interesting new data point on this card. I had this card set up so that there was an automatic $5 Amazon allowance deducted each month, and then autopaid each month afterwards. In the past, I always got the bonus. However, this past month (February 2017), although $5 was definitely charged to the card and showed up in my Amazon account, that charge simply vanished from my credit card account and did not show up at all on my February statement, leading to a $0 balance. I’m not sure if the bank did this on purpose to avoid paying my next quarterly bonus, but in any case, it meant I got $5 for free last month.

This has been discussed in the article above and elsewhere, that BOA will “forgive” around a $4 charge for this card to avoid paying the quarterly bonus. Apparently the (DP) mark is now $5. No other BOA card forgives charges AFAIK. So you got the $5 for free, but lost out on the $25-30 rewards for the quarter, which is a bust. I think a $10 monthly spend is a better bet – maybe more, since we are gaming the system by not truly carrying a monthly balance that was intended by the bank.

How does the quarter work? Does it follow the yearly quarter listed below? I recently did a product change which happened I think on Oct 17, 2016. Since then I’ve had 4 statements generated (NOV, DEC, JAN & FEB). When the product change happened, I called customer service to check when I would my quarterly bonus. I was told the quarterly bonus will be based from the date I received the card which means I should have received the bonus in FEB for NOV, DEC & JAN months. But I have not received anything yet. So, I again called customer service last week and now I am getting a different answer. Now they are saying it is based on the regular quarterly calendar listed below.

Q1 – JAN to MAR

Q2 – APR to JUN

Q3 – JUL to SEP

Q4 – OCT to DEC

I carry a balance when I can on this card. I’m almost sure the $30 algorithm is this:

1. If balance left is greater than the minimum payment -plus one- at closing cycle, then the bonus formula kick starts.

2. At 3-month interval, the system compares the carrying balances.Then, it deducts the 3 minimum payments -plus one- (ONE is whatever you pay over the minimum)

3. Finally, that equals a bonus of $10 x 3 months. (So next, gain, it CHECKS, COMPARES, REPEATS!

If bonus doesn’t work for you, review your account and find out what month they got the bonus last. Maybe the charges you make now are OUT of calculation. OR the minimum payment (plus one) is made 2 weeks before the due date. Also, consider that the minimum payment is a % of the current balance. That minimum payment can’t be GREATER than the balance or LOWER than itself.

I AM pretty sure that if you start a balance with $30 and pay $26 just before closing cycle, you’ll trigger the formula/bonus. Then, after that, try the $5.99 balance trick.

Those bank systems are triggered by percentages … AND those bank representatives rely on notes… Guess what? Notes can be miss interpreted. I found out that reps don’t know their own products at times. I recently requested to move credit from one card to another one. A rep told me it was not possible if any of the cards were only $500. Then I call a different number and a different rep told me THAT previous info was not true. I’m sure you guys can product change. Just try different a rep; the retention department, the customer service in another state, the night crew, or the account manager.

—P.S. I TYPE fast.

Just to put it out there, I have this card. But here is the catch, make sure whatever monthly statement you set, it should be greater than > $30, because in the month you get the bonus, if your statement is less than 30, after you get the credit, your balance would go to negative that means your statement for that month is 0, then you would miss one bonus out of the 4 bonus a year.

Or you can have the balance deposited to your bank instead, as noted in the post.

I believe this is one card where paying the balance prior to the close of billing cycle is not a good idea. Pretty sure the terms require there to be a balance due and then a minimum payment made each month in order to receive the bonus.

You are correct.