Update 10/24/24: Shutting down on 11/25.

Update 5/12/23: Paused new signups again

Update 3/8/23: They’ve brought back the Indexed Savings accounts and new customers can again signup for this account. Right now the rwate is 4.75% APY. Update 2/8/23: Seems this Indexed Savings account isn’t taking new customers anymore.

Original Post:

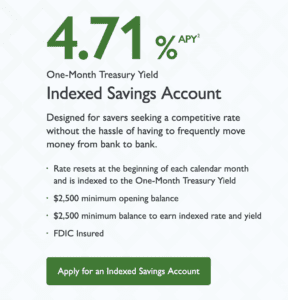

Ivy Bank Indexed Savings Account is a high yield savings account which is designed for savers seeking a competitive rate without the hassle of having to frequently move money from bank to bank. The rate resets at the beginning of each calendar month and is indexed to the One-Month Treasury Yield. It’s an FDIC-insured account with a $2,500 minimum and is available nationwide with the exception of California.

Direct Link to Ivy Bank Indexed Savings Account

Ivy Bank has been offering a high yield savings account, and I believe they’ve been doing a good job at keeping up with rate increases to match the top rates offered. (Maybe they are a CFG competitor for best simple high yield account?) This indexed account is a specialty product for someone who wants to rates matching the monthly Treasury yield.

This isn’t very different from buying U.S. Treasuries with auto-repurchase set up, if you are okay locking up funds for 30 days. There’s also another similar CD product from Merchants Bank which tracks the U.S. Treasury rates. This Ivy Bank account somehow seems simpler for someone who is more familiar with traditional savings accounts. Another advantage of this account is that the funds are not locked up at all.

One important downside to note: U.S. Treasuries are exempt from state and local taxes while this Ivy Bank account presumably is not exempt.

Personally I haven’t gotten around to doing any of these, and have been using a brokerage money market account which also more-or-less tracks the current Treasury rates since it’s mostly based on Treasury purchases.

Hat tip to andi

These sorts of gimmicks never last long or get much traction. For those who had this a yr or more and made a few extra bucks, thats great. Move it out.

Did anyone else get an email that they are “discontinuing our Indexed Savings account and will automatically transition your account to a High-Yield Savings account”?

For the first time since they established the account, the 3-month T-bill rate is consistently and appreciably below the 1-month T-bill rate. COINCIDENCE???

I THINK NOT!!!

Why? Isn’t their HYSA 5% as well?

5.62%/5.468%.

That was a pretty sweet average. This account was my number 3 in interest behind:

Superior Choice Credit Union- 7.25%APY/7% APR

Primis Novus – 6% APY/5.83% APR

Where’s the Superior Choice account you’re referring to? I can’t find it on their website.

Yep, the index account will be gone on 11/25/24. It would have been nice if they had kept it going considering rates are dropping, but at least they didn’t terminate it when rates were high.

true

Yeah, looks like this one’s over. It was a good run.

Are we staying or going? The Ivy HYSA 5.00% APY beats my money market mutual funds, but DoC’s HYSA list still shows banks with higher yields. The question is: Will they stay near the top of the list? One great thing about the Indexed Savings was not having to chase yields from account to account. And not having to make umpteen debit purchases, etc. to get a good rate. What will you do now?

that’s it. Shutting down on Nov 25. It’s been an excellent ride, though.

It looks the APY for November will be 5.053%

until Nov. 25

October 1st: 5.11% APR / 5.242% APY

Considering that the latest one month Treasury rate is only 4.87%, the 5.11% APR/5.242% APY for Ivy Indexed Savings in October is not bad at all. Of course, if Ivy does not lower its regular HYS on October 1 but stays at 5.30% APY, that’s even better – every penny counts!

Looking like a big drop for October.

5.18 as of 9/12. 4 more days to go…

yikes.. where is everyone moving their funds to after Ivy?

Nowhere. We seem to be entering an environment of moderately-high, but declining, interest rates. So I expect that, at any given moment, there will be a few HYSAs with a higher APY than this index-linked account. But all of these other HYSAs can have their APY cut by an arbitrarily large amount. So I expect that the collection of HYSAs with an APY higher than that of the Ivy Indexed account will be a rotating “cast.” I’d rather not chase the highest APY.

When do you guys anticipate the rate will start declining? just curious

Currently, CME Fedwatch says there’s a 76.5% chance that the Federal Reserve will cut the federal funds rate by 25 basis points and a 23.5% chance of a 50 bp cut. I expect the 1-month T-bill will generally follow as the Fed cuts rates.

thanks! is that for the FED meeting end of Sept?

Yes, I should have said that!

Absolutely! I was also checking the rate in the past few days and was pleasantly surprised by the jump which I would even call big (though largely meaningless like you said).

Edit: Wrote this in the wrong place. Was responding to PaulinTexas/lohengrin.

Good News!

Sep 1st – 5.53% APR / 5.685% APY

I know it’s largely meaningless, but it sure was nice to see that tiny jump today from the .48/.49 of the last 2 days, wasn’t it?

Thank you PaulinTexas for posting the rate every month.

I don’t know how this stuff works.

What happens when the FED starts lowing interest rates later this year and consequently banks lower their interest rate. Since this Ivy account is tied to treasuries? Does that mean the rate on this account will start to decline too? Thanks for any insight into this.. I’m a newb

The Fed funds rate set by the FOMC is, explicitly, only the rate that banks lend to each other. The interest rate of a 1-month T-bill, like any other security, is “set” by the buyers and sellers in the market. The 1-month t-bill is the shortest duration Treasury, so it almost always “follows” the Fed funds rate the closest. This savings account has an interest rate explicitly tied to the going interest rate of this ubiquitous short-term debt security. In contrast, almost every bank deposit account has an interest rate which is unilaterally set by its financial institution, and at most the interest rate that they decide is influenced by current interest rates for short-term debt securities.