Navy Federal Credit Union (NFCU) offers five different credit cards to it’s members. Readers of this site might be interested in these cards because some of them come with sign up bonuses and also have ongoing category bonuses.

Contents

Eligibility & Becoming A Member

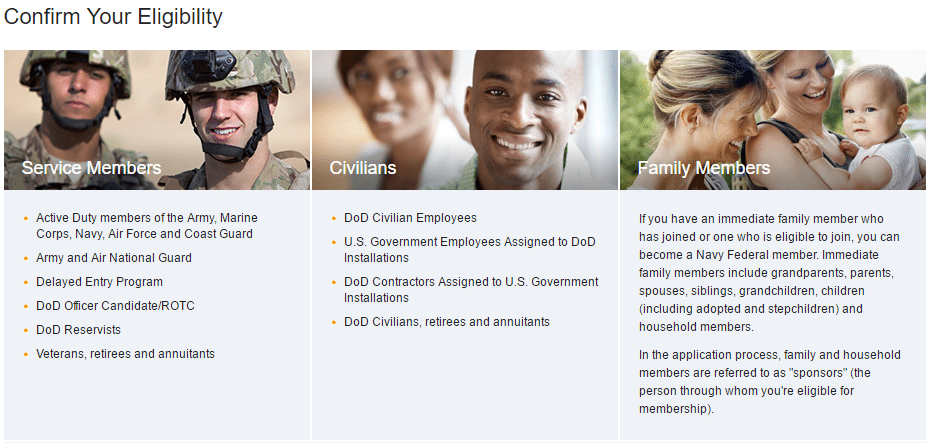

NFCU is a credit union with restricted membership. You can view the full eligibility requirements here.

There used to be a work around so that anybody could join, but that no longer works. From time to time they offer bonuses for becoming a member, currently you can get $50. It’s important to also remember that becoming a member results in a hard pull.

List Of Credit Cards

As mentioned, NFCU offers five different credit cards to it’s members. They are as follows:

- cashRewards

- GO REWARDS

- Visa Signature Flagship Rewards

- Platinum

- nRewards Secured

- American Express MoreRewards

Best Cards

There are only really two cards worth considering and they are:

- cashRewards:

- No annual fee

- Card earns 1.5% cash back on all purchases

- Sign up bonus of $200 cash back after $3,000 in spend currently

- Visa Signature Flagship Rewards

- Annual fee of $49 waived first year

- No foreign transaction fees

- Card earns 2x points per $1 spent

- Targeted bonus of 40,000 points after $3,000 in spend within the first 90 days of account opening

- MoreRewards:

- No annual fee

- Sign up bonus of up to 30,000 points (worth $300)

Current & Past Promotions

Current:

- Navy Federal cashRewards $200 Credit Card Bonus

- Double points at wholesale clubs

- Navy Federal Credit Union: Military Appreciation Month ($50 For Joining/Referring – Share Your Referrals)

- [Targeted] Navy Federal Flagship Rewards 40,000 Point Bonus

Past:

- Join Navy Federal Credit Union & Get $25 Bonus

- Navy Federal Flagship Rewards 30,000 Point Bonus

- Navy Federal Offering 2% Extra Cashback At Warehouse Clubs Until December 31st, 2016 (Up To 4x W/ No Cap)

- Navy Federal cashRewards Credit Card $200 Sign Up Bonus

- Navy Federal Increases Sign Up Bonus To $150 On cashRewards Credit Card

- Receive $10 For Enrolling Any Navy Federal Card With Visa Check Out

- [Military Only] Navy Federal Adds $150 Sign Up Bonus To GO Rewards Card

- Navy Federal Credit Union $100 IRA Bonus

- Navy Federal Increases Sign Up Bonus To $200 On cashRewards Credit Card

- [Expired] Navy Federal Credit Union Offer 5% CD On Balances Up To $5,000

- Visa Checkout: $15 When You Use A NFCU Card

Things You Should Know

- Credit limit increase requests are complicated. If you request a credit limit increase and it’s automatically approved, it will be a soft pull. If you request a credit limit increase and they counter with a lower limit it’s a soft pull. If you request a credit limit increase and are told you’ll be notified in 3-5 days a hard pull will be done. We explain this process in some detail here.

- They do not expedite sign up bonuses. In addition the bonus won’t post until after the spend period is over. For example if the card requires spending $1,000 within 90 days and you meet that within the first 30 days you’ll still need to wait for the full 90 days to pass to receive the sign up bonus.

- They do allow product changes between their different credit card products. No hard pull is done.

- They offer expedited shipping (at least on the Flagship rewards card) but it costs an extra $12.99.

- There is at least one data point of them not matching higher sign up bonuses when you’ve applied for a lower bonus recently.

Things We Want To Know

- If their cards are churnable

- If they combine inquiries when you apply for multiple cards in the same day

- How annual fee refunds work

- If there is a limit to the number of NFCU cards you can hold at one time

- Phone number for reconsideration

- If you can reallocate credit limits and if a soft/hard pull will be done

- If they will pull a different bureau if you have a frozen report

- If they allow product changes

- If they offer retention bonuses

- If you can change your statement closing date

If you know the answers to any of this, please share in the comments. Pages like this are as useful as readers make them, big thanks to all the readers who contribute.

We’ve done a similar post for other card issuers that you can view below:

- Alliant

- American Express

- Bank of America

- Barclaycard

- Capital One

- Chase

- Citi

- Comenity

- Discover

- Synchrony

- TD Bank

- US Bank

- Wells Fargo

I am interested in this card. I am a military spouse.

Something I want to know: has anyone used the Flagship CC to fund any bank account and had it count towards the spend req?

Bank account funding with an NFCU CC may or may not work for earning rewards, and therefore not count toward a SUB. No CA fee was assess, but the charge not earning anything is useless.

My DP’s:

In 2018, Andigo CU CC funding failed to work for earning points, but BBVA did work. (both of these FI’s have merged with other entities now)

https://www.doctorofcredit.com/targeted-navy-federal-flagship-rewards-40000-point-bonus/#comment-594152

In 2024, BluPeak CU funding failed to work for earning points.

https://www.doctorofcredit.com/ymmv-ca-only-use-credit-union-300-checking-bonus/#comment-1855248

If they aren’t going to earn points, I would rather a credit card just reject the transaction. Waste of time and effort.

Although you list “Is there is a limit to the number of NFCU cards you can hold at one time?” under “Things we want to know” I believe that is settled: only three Navy cards at a time. I have two at the moment and a very friendly and competent CSR confirmed the “only three Navy cards” rule yesterday.

I am about to apply for my third Flagship (I got the bonus both times before) and I will have a lot of helpful information I can post once I find out if I am approved and even more when I get the FS bonus again.

A fascinating but frustrating thing about Navy is that they have their own proprietary system that does not use FICO and depends in part on data that is not on your credit report, e.g. how much money you have in your Navy checking, how much in your Navy Savings, whether you have recurrent direct deposits set up, have you been regularly using any existing Navy cards. I discovered that the hard way when I applied for a Flagship 5 months ago and was declined. I had an 830 FICO 8, very low rent to income ratio, over 100k annual income. And I was still declined! They later showed me later my Navy proprietary score, which was sub-average, and listed some of the above items as reasons for decline.

Navy also looks into any property you own, whether you have a loan or out-right own it.

That surprises me. How would they know whether you own a boat, a car, a house (etc.) that you had paid cash for (and therefore there was no credit trail on any of your three reports tying you to owning it)?

I do understand the mechanism by which they could evaluate how much cash you have had in your Navy checking and savings over time, or whether you had been using your existing Navy credit cards each month, or whether you had DDs set up. All that is visible to Navy easily.

I had a similar experience getting rejected for flagship card last month, they cited balance status of navy fed accounts and no direct deposit at navy fed as reasons (along with no installment loan and recent hard pulls on credit)—they refused to provide any clarity about the first two points, would you mind detailing whether/how much you direct-deposit with them or keep in navy fed accounts? I want to know if it’s worth the trouble to try again later (only have basic member savings as I joined specifically for the card, which they declined, and the savings rate isn’t very good)

Happy to relate. I went full-bore on everything they mentioned. Namely I increased my checking balance and savings balance to a minimum daily balance of $1002 each. I made a small purchase on each of my existing NFCU cards and allowed them to report on the statement, then afterward paying them off. I also set up a recurring ACH transfer from an external bank to my checking account and a similar internal one from my NFCU checking to my NFCU savings, always keeping balances above $1002 dollars. Then I kept all that in place and waited 100 days before I applied again. (BTW, all of the above appear to be factors in their proprietary scoring model, according to my first rejection letter.)

It worked and I was awarded my Flagship card. As an aside, the Flagship is churnable. This was my third Flagship bonus. But you have to make sure you have at most 2 NFCU cards at the time you apply for your third.

also, I know you can have three cards with them as I know two people who do. per what I see from there data points from googling, it appears three is the limit. But I can vouch that you can have three at a time. Have not advised applying for a 4th without closing out one first.

5/24, 3/12,

EQ:761, TU:722 (frozen), EX:762

Responded 12/23/21 to a preapproved Flagship mailer for 50k/$4k/no AF offer. Had TU frozen, which they attempted to pull. Got a “We’ve received your application for a FLAGSHIP REWARDS card and will review it as soon as possible. You can expect an answer within 24-48 hours.”

It seems that preapproval might be based on one specific bureau? I assume I got that language because my frozen TU and they’ll pull EQ or EX before deciding. will update when I find out more

DP: Cannot get more than one NFCU CC approval on the same day, or even within a 3 month period. So, it’s impossible to combine HP’s. Personal cards anyway – not sure about Biz.

I cannot remember where I saw it, but saw a DP recently where someone had called to recon and NFCU said you cannot get more than one card in a 90 day period. I tested it and believe it to be true. I think this guy knows this is true: Dan - Legal Bank Robber

Dan - Legal Bank Robber

09/30/2019 – Applied and instant approved for MoreRewards Amex TU HP in VA.

12/10/2019 – Applied for CashRewards online. No HP took place. Instant denial. Error said I did not meet “underwriting criteria”. Snail mail letter a week later said “we are unable to approve your application for the following reason: YOUR RECENTLY APPROVED NAVY FEDERAL CREDIT CARD ACCOUNT IS TOO NEW”.

01/02/2020 – Applied and instant approved for CashRewards. TU HP in VA.

Previous card with them was Flagship from May 2018 – May 2019. Too afraid to try to churn the Flagship so I settled for a $250 bonus on the CashRewards. Still waiting on the MoreRewards bonus to post.

Correct

Hi Dan. Does this 90-day rule apply to Navy cards only? In other words, if I applied and was approved for a non-Navy card 75 days ago and that fact shows on my TU report, that would not in itself trigger the 90-day rule — correct?

No, this rule is only for Navy Cards. You are fine to apply.

See my question to Dan below regarding the 90-day rule.

I recieved an email with a link to access my card number the day after I was approved.

A phone customer service representative said you have to wait 90 days after joining the credit union to be approved for a card. They also said that beginning on August 26, 2019 you can call in to see if you are pre-approved for any of the cards (This can only be done over the phone).

This is no longer true. I joined and got the Flagship card the same day. They sent me a funny letter that read like a denial. It said they gave me a high rate because of my lack of relationship with them. Who cares?

NFCU data points 7/2/2019:

Called to cancel Flagship rewards 4 days after annual fee posted.

They recommended a product change to keep my credit limit

They will waive the fee, but state it will be few days before it comes off. A supervisor had to be asked to waive the fee – which was done while I was on the phone.

They allowed me to choose if I wanted a Visa or MC cash rewards card (the product I switched to)

Data Point: called my nfcu rep (idk she called me shortly after being approved for membership) and did the app for the signature rewards card via phone and she was able to waive the 12.99 expedited shipping fee.