I think the two are unrelated. Plastiq isn’t paying out Nearside’s cashback. Plastiq recently went through a mini-overhaul and I think a revamp of their fee schedule is part of how they’re paying for it.

Yes they are. Exempt Debits(like Nearside) can charge way higher fees and you aren’t legally allowed to discriminate against them compared to regular debits. This is why it is hard to get money order machines hard coded against gift cards without working with the issuer and having it done on their side.

I’m assuming Plastiq didn’t see enough people paying with actual debits to make the 1% profitable

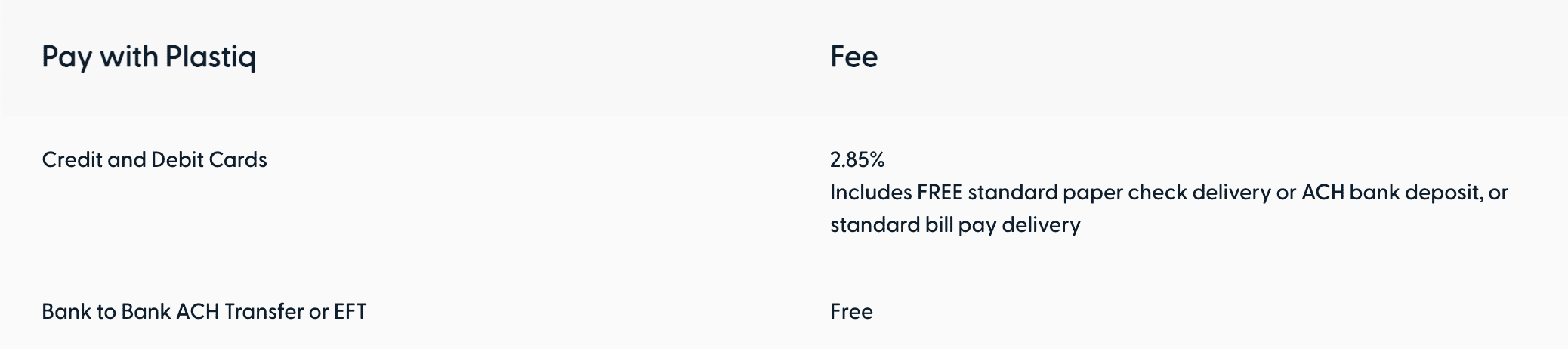

Plastiq charges 2.85% for “debit cards issued by online-only banks” per their terms. Nearside never worked, at least not for me. 2.85% fee was charged with each transaction.

I used Nearside Debit several times on Plastiq with a 1% fee. I feel very fortunate now that I scheduled some recurring payments with Nearside on Plastiq and because they were scheduled before the fee increase, they still show 1%. (Knock on wood)

They did not get canceled and are still processing at 1%. Plastiq has always honored the fee at the time the payment was scheduled for me. We’ll see how long it lasts, but all late March payments went through at 1% as scheduled after this change went into effect.

Ash (@guest_1348951)

March 16, 2022 17:16

#1348951

Crazy. Debit card fee for processors are just 15 basis points.

Bob (@guest_1348896)

March 16, 2022 16:01

#1348896

*Checks calendar*….*It’s not April 1st*

Wow these f**kers. I literally just got the cashback debit card I wanted for this.

I am. While not the slam dunk it used to be, I value returns on SUBs and some rewards at well over 3% of spend and for some payees that don’t accept CCs, I’m fine with just a bit over break even for the convenience.

I am gladly paying the 2.85% as it is a business expense deduction and i am getting miles and points so buying miles and points way cheaper then when airlines/hotels sell them even at a 50% discount off inflated values.

If it’s a personal expense it makes a difference but as a business expense you either have to pay taxes on the rewards or reduce your cost of good based on the value of the rewards so either way your paying for it there is no magic you can do to get around that

For a business expense deduction, you’re required to reduce the amount of the deduction by what the points/miles are worth. Doesn’t mean you’ll get caught, but that is how you’re supposed to do it.

I’m not a tax professional, but you can confirm this with someone who is.

I think I will. I have 4% cash back debit crypto card. The volatility makes it iffy but to pay bills that don’t take credit cards, I think it might be worth the risk. Although I am pretty sure CoinB (card issuer) might shut me down. So far I only have been doing about $3k per month. The limit is only $1,500 per day. I have been going slow hoping to build dup to 1,500 per day. After fees its about $30 per day. I think I will try until they shut me down.

Plastiq isn’t going anywhere. Plenty of real businesses use the service. Once they cut out the churners and abusers they’ll be more profitable than ever.

People using debit cards didn’t cost them money. People using credit cards for minimum spend paid the 2.85% fee. I fail to see how you think Plastiq was losing here. All fees were being paid by the customer.

Now 2.9% as of 12/1/22

They sent an email saying they plan to go public. Look out for freebies/offers/FFDs until the date they go public as they will want to drum it up.

2.85% is ridiculous when I can pay taxes for 2.3% or less.

It’s not so bad to pay rent for SUB MSR when it’s one of only options.

Welp. There goes 1.2% cashback on Plastiq with Nearside… :/

I think that’s what killed it tbh, neobanks offering >1% on debit cards

I think the two are unrelated. Plastiq isn’t paying out Nearside’s cashback. Plastiq recently went through a mini-overhaul and I think a revamp of their fee schedule is part of how they’re paying for it.

Yes they are. Exempt Debits(like Nearside) can charge way higher fees and you aren’t legally allowed to discriminate against them compared to regular debits. This is why it is hard to get money order machines hard coded against gift cards without working with the issuer and having it done on their side.

I’m assuming Plastiq didn’t see enough people paying with actual debits to make the 1% profitable

Plastiq charges 2.85% for “debit cards issued by online-only banks” per their terms. Nearside never worked, at least not for me. 2.85% fee was charged with each transaction.

I used Nearside Debit several times on Plastiq with a 1% fee. I feel very fortunate now that I scheduled some recurring payments with Nearside on Plastiq and because they were scheduled before the fee increase, they still show 1%. (Knock on wood)

They’ll get cancelled dw. Plastiq hasn’t honored old pricing in the past.

Plastiq has always honored posted fee on my recurring payments. I do hope my 1% sticks, It is still processing as of yesterday.

They did not get canceled and are still processing at 1%. Plastiq has always honored the fee at the time the payment was scheduled for me. We’ll see how long it lasts, but all late March payments went through at 1% as scheduled after this change went into effect.

Crazy. Debit card fee for processors are just 15 basis points.

*Checks calendar*….*It’s not April 1st*

Wow these f**kers. I literally just got the cashback debit card I wanted for this.

Same.

Why use a bank-issued debit card with Plastiq when I could just use the bank’s own BP system. For free.

lmao ….who is paying 2.85% fee

I am. While not the slam dunk it used to be, I value returns on SUBs and some rewards at well over 3% of spend and for some payees that don’t accept CCs, I’m fine with just a bit over break even for the convenience.

For debit…

I am gladly paying the 2.85% as it is a business expense deduction and i am getting miles and points so buying miles and points way cheaper then when airlines/hotels sell them even at a 50% discount off inflated values.

You still need to pay taxes on the earned points/miles right?

IRS does not consider points/miles taxable, they’re considered a rebate.

no- google it and read up on the US Court/IRS case where it is deemed a rebate. No taxes

Anikeev vs Commissioner for rebates as long as it’s not a cash equivalent.

If it’s a personal expense it makes a difference but as a business expense you either have to pay taxes on the rewards or reduce your cost of good based on the value of the rewards so either way your paying for it there is no magic you can do to get around that

That’s for personal purchases.

For a business expense deduction, you’re required to reduce the amount of the deduction by what the points/miles are worth. Doesn’t mean you’ll get caught, but that is how you’re supposed to do it.

I’m not a tax professional, but you can confirm this with someone who is.

I think I will. I have 4% cash back debit crypto card. The volatility makes it iffy but to pay bills that don’t take credit cards, I think it might be worth the risk. Although I am pretty sure CoinB (card issuer) might shut me down. So far I only have been doing about $3k per month. The limit is only $1,500 per day. I have been going slow hoping to build dup to 1,500 per day. After fees its about $30 per day. I think I will try until they shut me down.

I thought the limit was $2500/day. Also does Plastiq still accept Coinbase card? I thought they didn’t anymore.

I give Plastiq 18 months before it stops operations.

Plastiq isn’t going anywhere. Plenty of real businesses use the service. Once they cut out the churners and abusers they’ll be more profitable than ever.

People using debit cards didn’t cost them money. People using credit cards for minimum spend paid the 2.85% fee. I fail to see how you think Plastiq was losing here. All fees were being paid by the customer.

who knew the ceo of plastiq was on DOC?

Well, there go all the debit MS plays.

I guess for the people that like to run mastercards for mortgages etc for a SUB it still works. As for me, i’m out. Adios!

2.85 IS HIGHER THAN MOST SURCHARGES. THE KISS OF DEATH