Update 7/9/26: Extended until October 6, 2026

Update 4/8/26: Extended until July 7, 2026.

Update 1/8/26: Valid again from 1/7/26 through 4/6/26 at this link (ht catcat). The tiers are slightly different now, updated below.

Update 10/26/25: Extended through 1/6/26 (ht reader Lin)

Update 7/8/25: Deal is back through September 30, tiers seem to be different this time.

Offer at a glance

- Maximum bonus amount: $2,000

- Availability: Must open in branch [Branch locator]

- Direct deposit required: No

- Additional requirements: Deposit up to $200,000

- Hard/soft pull: Soft pull

- ChexSystems: Unknown

- Credit card funding: None

- Monthly fees: $15, avoidable

- Early account termination fee: None

- Household limit: None listed

- Expiration date:

December 31st, 2019June 30, 2021

Contents

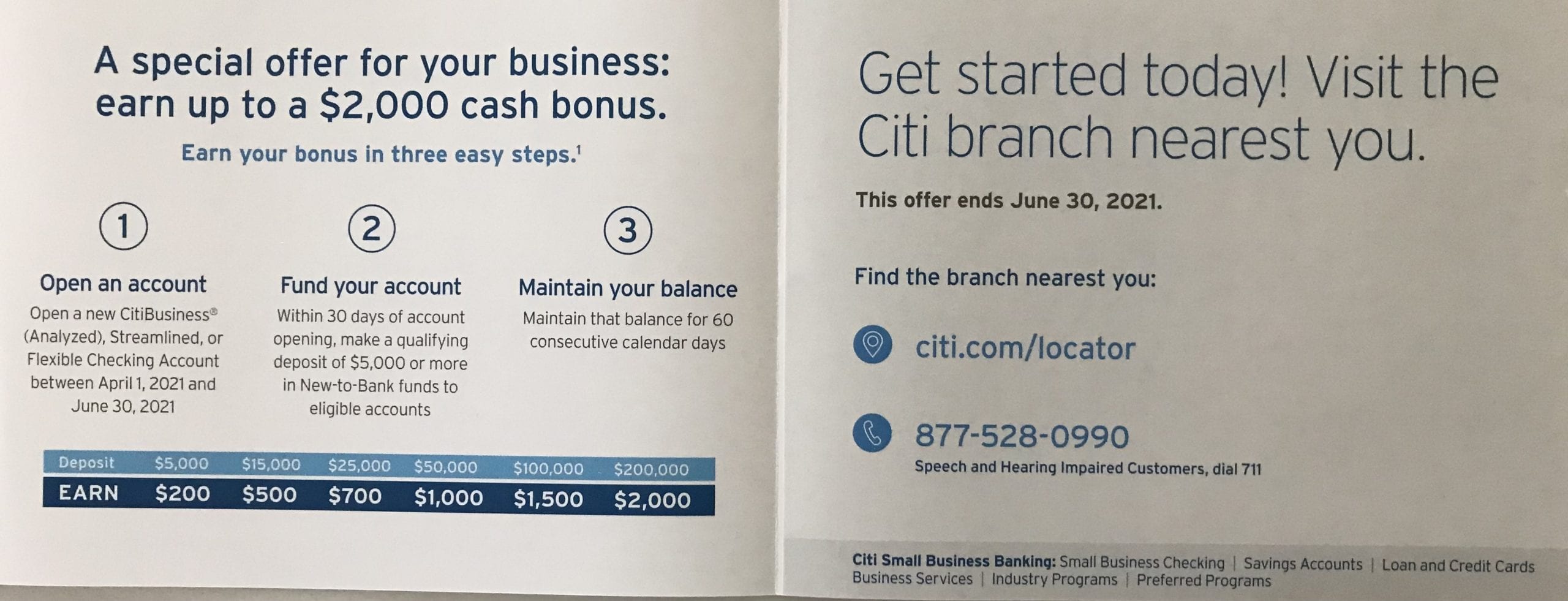

The Offer

No direct link, being offered in branch

- Citibank Business is offering a bonus of up to $2,000 when you open a new business checking account. The bonus you receive depends on how much you deposit, balance must be maintained for 60 calendar days after deposit.

- Receive a $300 bonus with a $5,000 deposit

- Receive a $500 bonus with a $20,000 deposit

- Receive a $1,000 bonus with a $50,000 deposit

- Receive a $1,500 bonus with a $100,000 deposit

- Receive a $2,000 bonus with a $200,000 deposit

The Fine Print

- All bank account bonuses are treated as income/interest and as such you have to pay taxes on them

Avoiding Fees

Monthly Fees

The easiest account to keep fee free is the CitiBusiness®Streamlined Checking Account, this has a monthly fee of $15 and is waived have an average monthly balance of $5,000 or more.

Early Account Termination Fee

There is no early account termination fee to worry about.

Our Verdict

Reader Jay was able to get this offer just by going into a branch and asking if they had any current promotions for opening a new account. Entirely possible it won’t be available in all/most branches, but feel free to share your data points in the comments below. Similar to a previous targeted bonus, with higher tiers available as well. The return gets worse as the bonus increases as unfortunately. Will stack with the Lunar new year promotion as well.

Useful posts regarding bank bonuses:

- A Beginners Guide To Bank Account Bonuses

- Bank Account Quick Reference Table (Spreadsheet) (very useful for sorting bonuses by different parameters)

- PSA: Don’t Call The Bank

- Introduction To ChexSystems

- Banks & Credit Unions That Are ChexSystems Inquiry Sensitive

- What Banks & Credit Unions Do/Don’t Pull ChexSystems?

- How To Use Our Direct Deposit Page For Bank Bonuses Page

- Common Bank Bonus Misconceptions + Why You Should Give Them A Go

- How Many Bank Accounts Can I Safely Open Within A Year For Bank Bonus Purposes?

- Affiliate Links & Bank Bonuses – We Won’t Be Using Them

- Complete List Of Ways To Close Bank Accounts At Each Bank

- Banks That Allow/Don’t Allow Out Of State Checking Applications

- Bank Bonus Posting Times

Post history:

- Update 1/19/25: Deal is back until July 7th 2025.

- Update 7/11/24: Deal is back until 1/7/2025. Funds only need to be maintained for 45 days. Hat tip to Erik

- Update 6/24/24: Valid until July 8

- Update 11/22/23:Still have to open in branch, just lets you input information online

Deal is now available online.Hat tip to Adam D - Update 10/5/23: Extended until January 9, 2024.

- Update 7/13/23: Deal is back and valid until October 4, 2023.

- Update 1/5/23: Extended until 7/12/2023. Can try this direct link.

- Update 7/6/22: Extended until January 4, 2023.

- Update 1/21/22: There is now a direct link for the offer.

- Update 1/5/22: Extended through 7/5.

- Update 10/4/21: Extended through 1/3/22.

- Update 7/2/21: Extended until 9/30/21.

- Update 4/30/21: There is now a direct link for this offer.

- Update 4/8/21: Deal has been extended until June 30, 2021. Hat tip to reader EW

- Update 1/28/21: Deal is back and valid until 3/31/21. Hat tip to reader EW

- Update 9/23/20: Deal is back and valid until 1/5/2021. Hat tip to reader KJ Z

- Update 1/10/2020: Deal has been extended to March 31st, 2020 as per reader B